Concentration Risk: How To Efficiently Manage Employee Equity & Compensation Risk

In a perfect world, logic would always guide our financial decisions. Emotions wouldn’t come into play.

But we don’t live in a perfect world. Far from it.

That means our emotions impact our financial choices more than we realize.1

Shockingly as much as 95% of our purchase choices are made subconsciously, driven by our emotions—as little as 5% are based in logic (and that’s when we’re in a good head-space and feeling comfortable and secure).2

When we’re faced with uncertainty, fear and instinct can take over and push logic right out of the window.3

Your brain will make you want to react quickly to protect yourself and avoid the pain you anticipate from potential losses.4

Ironically, these instincts often make things worse. Emotional reactions can lead to poor choices and the losses you were trying to avoid in the first place.5

The best way to avoid letting your hardwired biases take over? Use these strategies. They can help you fare better in any crisis. They may even make you a savvier investor.

Overconfidence is a killer. In fact, research shows that the more experience you have as an investor, the more overconfident you tend to be.6

Stay realistic and grounded by a strategy. Get advice before making big decisions.

Losing money hurts. The truth is that the pain of losses can actually be more intense than any satisfaction from gains. Economists call that “loss aversion.”7 The pressure of anxiety or uncertainty can lead to irrational choices that actually work against our big-picture financial goals.

Don’t give into fear or panic when they show up. Focus on logic and rely on your professional for guidance.

Framing is everything when it comes to evaluating performance. That’s because the way information and events are presented to us can sway our perception and influence our decisions.8

Look beyond short-term outcomes when framing performance. Think about your longer-term goals and the progress you are making towards them, even when short-term corrections slow your progress.

Recent events usually influence you more than those in the distant past. Why? The human brain remembers recent events more clearly and gives them outsized weight when making decisions. Your brain can mislead you by expecting more of what you’ve seen already. And that can lead to overconfidence and emotional decisions.9

Resist this tendency by remembering the market is constantly changing. Over the long term, bear markets recover. And no bull market lasts forever.

With decision making, it’s natural to focus on one aspect or one piece of information as a starting point. Often, that can greatly influence your final choice. This is known as “anchoring bias,” which can give you tunnel vision. It can lead you to fixate on a single data point, like an investment’s price, while ignoring other key information.

To fight it, seek out more information. Think critically about multiple perspectives, and don’t forget to consider future potential.

Humans like to make snap decisions. And, when you’re stressed out, you’re far more likely to make impulsive decisions. The problem is that “gut” decisions are made based on instinct, habit, and emotions, instead of logic and facts. When you’re in gut-decision mode, it can be much harder to make goal-oriented choices.10

Take your time when making financial decisions and let your brain shift into analytical mode. With a little time, emotions cool down, and you’ll typically consider more alternatives.11

We can’t foresee or control downturns or upswings. We can only control our mindset, our emotions, and our financial choices.

Markets and economies are never predictable or under our control. We can’t foresee or control downturns or upswings. We can only control our mindset, our emotions, and our financial choices.

That’s easy to lose sight of during periods of economic uncertainty and financial stress.

But, if you can focus on the long game and improve your mental game, you’ll come out stronger and more prepared.

That can make you less vulnerable to hardwired human biases and help you make better financial decisions, no matter what the markets are doing.

As a financial adviser, one of my most important jobs is to help you become a smarter, more capable investor. That involves using psychology and behavioral finance to help you learn more about how your brain works and improve your financial behaviors.

I’m also here to be an objective accountability partner. I talk my clients through emotional decisions, and I can be an important voice of reason and calm when markets are turbulent and it feels like the sky is falling.

If you’re curious about behavioral finance—or if you need a sounding board for a financial decision—I’m here for you. Don’t hesitate to call me at 800-840-5946.

I’d be happy to answer your questions and share some more advice.

No matter what they are, they’re guiding your financial choices. And they’ve already shaped your financial habits.

This month, we’re exploring the importance of your money mindset and sharing some exercises to help you understand more about it.

The more you know about your money mindset, the more you’ll know about yourself — and how your mindset affects your financial decisions and your overall financial health.

Go ahead and click here to learn more about your money mindset.

Risk Disclosures: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. The S&P 500 is an unmanaged composite index considered to be representative of the U.S. stock market in general. All index returns exclude reinvested dividends and interest. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. For illustrative purposes only.

Did you know that humans are twice as concerned about avoiding losses as they are about achieving investing gains?

That means investment losses hurt a lot.

You’ve probably heard that the worst thing you can do during a downturn is sell, but did you know the psychology behind that impulse? It’s called loss aversion.

It’s one of the reasons why people can sabotage their investments by selling when they get scared, missing the recovery, and then buying back in once they feel “safe” again.

Understanding and leveraging human psychology is one of my most important jobs as an adviser.

My approach uses the Risk Number®, based on Nobel Prize-winning research. Together we can quantify how much risk you want, how much risk you currently have, how much risk you need to reach your goals, and how much risk you should take on.

Your Risk Number® is like a speed limit. Some people are comfortable driving fast while others want to go slower.

I’d like to help you determine your comfort zone and use it to manage your investments so you can rest assured that your investment strategy truly reflects your Risk Number®.

Discover Your Risk Number® and find out if your current investment strategy truly reflects your risk tolerance (and for many people, it doesn’t).

Risk Disclosures: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. The S&P 500 is an unmanaged composite index considered to be representative of the U.S. stock market in general. All index returns exclude reinvested dividends and interest. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. For illustrative purposes only.

The discussion around marijuana has undergone great social, legal, and economic changes in the last few years: From Reefer Madness to hot new investing fad.

Think marijuana is missing from your portfolio? Read this first…

Richard Archer is a financial advisor and the President of Archer Investment Management with more than twenty years of industry experience. He specializes in providing comprehensive financial planning and investment guidance and personalized care and attention to professionals with complex compensation and families pursuing financial freedom. Along with holding a Wharton Bachelor of Science in Economics and a Texas MBA, he is a CERTIFIED FINANCIAL PLANNER™ and a Chartered Financial Analyst®. He combines his advanced industry education and knowledge with his genuine care for people to provide clients with an exceptional experience. To learn more about Richard, connect with him on LinkedIn, Facebook, Twitter or visit www.archerim.com.

What kind of investor are you? We broke down your investing mindset into 7 questions to show how your personality can lead to investing extremes. You can download and take it right here.

Self-knowledge is power.

Here’s an example of what you’ll learn:

Are you the kind of person who reads the financial headlines every day or do your financial statements pile up on the counter?

It all depends on your personality. My quiz can help you discover your own mindset in just 7 questions.

You might think that more information is always better, but it’s actually a balancing act.

Getting into the details too much can cause anxiety and take up time that you could be using for other purposes.

Ignoring your finances completely puts you at the other end of the spectrum — passive and potentially out of touch.

Where do you fall on that spectrum? Take our investing personality quiz to find out what biases you have and what they mean for your investing.

I think you’ll be glad you did.

Richard Archer is a financial advisor and the President of Archer Investment Management with more than twenty years of industry experience. He specializes in providing comprehensive financial planning and investment guidance and personalized care and attention to professionals with complex compensation and families pursuing financial freedom. Along with holding a Wharton Bachelor of Science in Economics and a Texas MBA, he is a CERTIFIED FINANCIAL PLANNER™ and a Chartered Financial Analyst®. He combines his advanced industry education and knowledge with his genuine care for people to provide clients with an exceptional experience. To learn more about Richard, connect with him on LinkedIn, Facebook, Twitter or visit www.archerim.com.

Have you ever considered the impact your investments make? Have you looked at the companies in which you’re investing and considered how they contribute to global problems or solutions? If you’ve wanted your investments to align with your values, you’re not alone. You just might not realize there’s a way to do so.

Socially responsible investing (also known as sustainable, ethical, or conscious investing) is an investment strategy that aims to consider both financial return and social good to inspire social change. Think of it as an opportunity for doing well while doing good. Socially responsible investing, or SRI, has increased in popularity over the years, growing 76% between 2012 and 2014 from $3.74 trillion to $6.57 trillion assets, according to Envestnet PMC.

Particularly since the Trump presidency and a slew of government policy changes, demand for SRI has continued to steadily increase. Additionally, Millennials have shown significant interest in SRI, which has contributed to the growth. Investors want to be able to invest in companies that support issues they care about, whether that’s social programs, education, or the environment. Individuals investors can essentially target their concerns through their investment behavior and consumption decisions.

Investing in companies that support causes you care about while also generating returns is appealing to many investors, which is likely why SRI has steadily increased. However, opinions are still mixed about the impact of SRI strategies on performance. Some studies claim that socially responsible investments don’t perform as well as traditional stock market funds. Additionally, some of these investments come with higher annual fees. And, depending on the type of company in which you wish to invest, such as wind, solar, or other alternative energy funds, you may face more volatility.

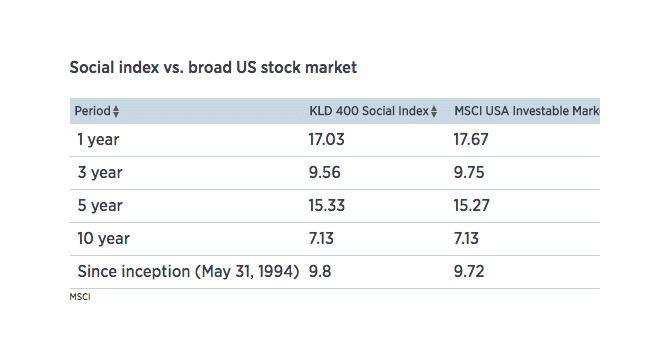

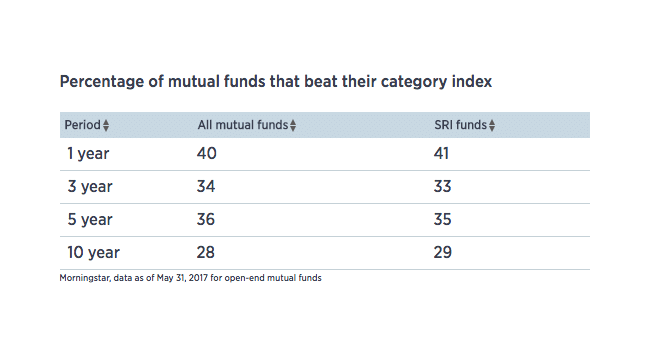

Morningstar reports that the average U.S. SRI mutual fund trails the benchmark S&P 500 index, but many funds that don’t fall into the SRI category have also fallen behind the market. As you can see, the jury is still out on whether or not sustainable portfolios experience a performance penalty.

Generally speaking, professionals recommend identifying reasons to invest in a stock, rather than focus on avoiding ones you don’t align with. Instead of focusing on stocks you don’t want to invest in, research those that you want to support.

Like any financial strategy, balance is key. Depending on your specific goals, you can incorporate SRIs into your portfolio. This gives you the opportunity to generate returns and save for your future while also supporting companies with social missions that align with your values.

The first place to start is to speak with a financial advisor and discuss your investment goals, your social values, and how they can integrate. At Archer Investment Management, our investment approach is disciplined, unemotional, and highly diversified and we favor objective advice to “hot stocks” of the moment. The philosophy we follow is based on the science of investing that drowns out the noise of the media and focuses on time-tested and thoroughly-researched strategies that have been proven to drive returns, reduce volatility, and simplify the investment process.

Providing comprehensive investment guidance, we can help you evaluate your SRI opportunities. For a complimentary portfolio review, contact our office at 800-840-5946 or click here to schedule a phone call.

Richard Archer is a financial advisor and the President of Archer Investment Management with more than eighteen years of industry experience. Largely working with successful individuals and couples, he specializes in providing comprehensive investment guidance and personalized care and attention to each client. Along with holding a Bachelor of Science in Economics and a MBA, he is a CERTIFIED FINANCIAL PLANNER™ certificant and a Chartered Financial Analyst®. He combines his advanced industry education and knowledge with his genuine care for people to provide clients with an exceptional experience. To learn more about Richard, connect with him on LinkedIn or visit www.archerim.com.

Have you ever ridden a touring bicycle down a mountain? I wouldn’t recommend it. Touring bikes are designed for paved roads, so shock absorbers are eliminated to make them lighter and pedal more efficiently.

If you took a touring bike down a mountain, you would end up in a lot of pain. For something like that, you need a mountain bike. They are designed with shock absorbers to cushion the impact of the rocks, logs, ditches and other obstacles you will inevitably confront on the trails.

Sometimes investors feel like they are riding a touring bike down a rough mountain. Every bump in the markets makes them want to cry out in pain, and they wonder if they’ll ever make it to their final destination. Why is this?

One thing that can make for a really jarring ride is having an undiversified portfolio. If your investments are highly concentrated, every little dip in the markets will be magnified and leave you reeling.

Another thing that will make for a really choppy ride is constantly changing asset allocations based on short-term rough patches in the markets. If you let every market pothole throw you off your bike, you’ll never get anywhere.

So, how can you smooth out your ride? What shock absorbers can you add to your bike to get you down the investment mountain in one piece and enjoy the ride?

Diversification. Spreading your portfolio across different securities, sectors, and countries will even things out and make for a much more comfortable, safe, and enjoyable ride. You will need to identify the right mix of investments, like stocks, bonds, or real estate, that align with your risk tolerance. This will keep you on track toward your goals no matter the obstacles that crop up.

You may not end up with the top performing portfolio, but you definitely won’t have the worst either. This strategy isn’t about being the best, it’s about creating a smooth enough ride for you to hang on until you get to the bottom of the hill. Without these shock absorbers, you are likely to quit halfway down.

Just as you would try to swerve around everything possible if you were riding a touring bike down a mountain, people with concentrated portfolios resort to market timing and constant trading in an attempt to anticipate the top-performing countries, asset classes, and securities.

This is nearly impossible. Here’s an example of just how unpredictable the ride can be. Among developed markets, Denmark was number one in US dollar terms in 2015 with a return of more than 23%. But if you had bet big on that country the following year, you would have ended up in a ditch. In 2016, Denmark slid to the bottom of the table with a loss of nearly 16%.

Even the US stock market, which is the world’s biggest, can throw you for a loop. It has been a strong performer in recent years, holding the number three position among developed markets in 2011 and 2013, first in 2014, and sixth in 2016. But a decade ago, in 2004 and 2006, it was the second worst-performing developed market in the world.

Trying to predict which part of a market will do best over a given period is also challenging. For example, while there is a plethora of evidence to support why we should expect positive premiums from small cap, low relative price, and high profitability stocks, these premiums are not laid out evenly or predictably across the map. US small cap stocks were among the top performers in 2016 with a return of more than 21%. A year before, their results looked relatively disappointing with a loss of more than 4%. International small cap stocks had their turn in the sun in 2015, topping the performance tables with a return of just below 6%. But the year before that, they were the second worst with a loss of 5%.

If you’ve ever ridden down a mountain, you know to expect the unexpected. There may be a rut or rock pile hiding just around the next turn. It’s important to have a bike with proper shock absorbers to handle whatever may come. Diversification isn’t some kind of magic that will make everything a perfectly smooth ride. But, it does smooth things out so that no individual investment will throw you off your bike. There will still be bumps along the way, but nothing that will keep you from reaching your goals.

Take a look at your portfolio. Does your investment bike need some shock absorbers? You’ve come to the right place because I’m an investment mechanic! With sufficient diversification, the jarring effects of performance extremes level out. Then, you will be able to hang on and enjoy the ride all the way to your investment destination. Click here to schedule a phone call, and we can get your portfolio ready for whatever lies around the next turn in the trail.

Richard Archer is a financial advisor and the President of Archer Investment Management with more than eighteen years of industry experience. Largely working with successful individuals and couples, he specializes in providing comprehensive investment guidance and personalized care and attention to each client. Along with holding a Bachelor of Science in Economics and a MBA, he is a CERTIFIED FINANCIAL PLANNER™ certificant and a Chartered Financial Analyst®. He combines his advanced industry education and knowledge with his genuine care for people to provide clients with an exceptional experience. To learn more about Richard, connect with him on LinkedIn or visit www.archerim.com.

Twingo. Clio. Polo. Ibiza. Do you know what these are? Maybe Caribbean islands? Possibly the names of Angelina Jolie’s children? Surprisingly, these are the most popular cars on the Spanish island of Tenerife, 90 miles north of Morocco. I only know this because I tallied them as they passed me on my four-hour bicycle ascent up the famous mountain El Teide.

I consider myself a “car guy,” yet I had never heard of these cars. I find that the more I travel, the more my eyes are opened to the fact that there are people living very different lives from mine who have valuable perspectives. This simple car analogy reminds me that I need to travel more and expand my viewpoints and knowledge beyond my everyday life in Austin, Texas.

It’s easy to think I’ve got everything figured out. I know where I want to live, what I like to eat, and the best places to ride. But that’s not the reality. Those things may be comfortable and familiar, but I keep finding new favorite things in new places. For example, Gran Canaria has the most difficult climbing in the world (not Boulder, CO), and I might like speaking Spanish more than English because it flows better!

This past election brought up plenty of talk about our personal “bubbles,” but many of us don’t take the time and effort to recognize our own bubbles that we base everything else on. It takes habit and discipline to look at things from a different perspective and learn other ways to do things.

For example, at one of my nightly team dinners, I sat near a Brazilian couple and listened attentively as they took me for a personal tour of South America. As I heard their thoughts, my limited life bubble seemed in stark contrast to their worldliness, and my preconceived notions were challenged. In their minds, Brazil is the “America” of South America, big and diverse with the best beaches in the northern part of the country (please don’t let this secret out!). Argentina is like France, where residents feel culturally elite and more refined than their South American neighbors; and Chile is most like Canada, friendly and inviting. Now that I know more about South America from their point of view, it feels less daunting for me to travel there, and Chile may show up on a future itinerary of mine.

It was fascinating to hear them thoroughly discuss a topic I had never taken the time to consider. I quickly learned that my worldview is greatly limited by my lack of experience. Just like most of us, I tend to favor the familiar and fear the foreign because I don’t know any differently. America is the best at everything after all, right? This concept goes beyond travel, it relates to your portfolio as well.

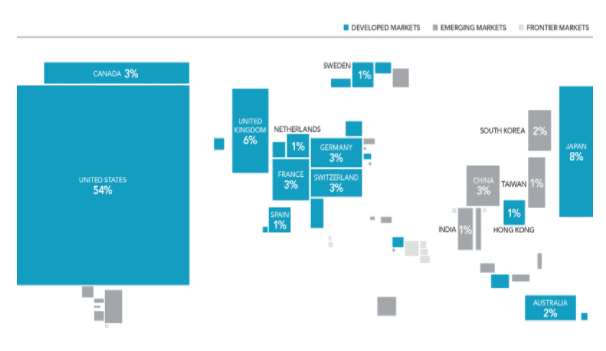

When I was a young investor, my portfolio leaned heavily towards familiar U.S.-based investments. In my mind, they were certainly less risky than unfamiliar foreign holdings. But I soon learned that there is a world of opportunity in equities. Did you know that the weight of the U.S. stock market relative to the global market is approximately 54%? As shown below, nearly half of the world’s investment opportunities are outside of the U.S., with non-U.S. stocks representing more than 10,000 companies in over 40 countries.

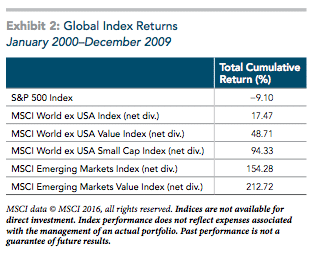

Although U.S. stocks have been in favor the last few years, this has not always been the case. January 2000 – December 2009 is known as the “Lost Decade” because U.S.-only investors lost money cumulatively over those 10 years. Here’s a look at how the market played out during that period:

Exhibit 2: Global Index Returns January 2000–December 2009

Over the last 20 calendar years, the U.S. has been the best performing country twice, and the worst performing country once. Global diversification implies that an investor’s portfolio is unlikely to be the best or worst performing, instead providing the means to achieve a more consistent outcome. It helps reduce and manage catastrophic losses that can be associated with investing in just a small number of stocks or a single country.

It’s important for us to expand ourselves with new experiences and knowledge as well as seek diversification in our portfolios. Not only does it improve our quality of life, but it also makes us more understanding of others and lessens extremes. If you are curious about global markets or worried that your portfolio isn’t globally diversified enough, I’d love to talk to you. Click here to schedule a phone call. To close, te veré en Santiago (I’ll see you in Santiago)!

Richard Archer is a financial advisor and the President of Archer Investment Management with more than eighteen years of industry experience. Largely working with successful individuals and couples, he specializes in providing comprehensive investment guidance and personalized care and attention to each client. Along with holding a Bachelor of Science in Economics and a MBA, he is a CERTIFIED FINANCIAL PLANNER™ certificant and a Chartered Financial Analyst®. He combines his advanced industry education and knowledge with his genuine care for people to provide clients with an exceptional experience. To learn more about Richard, connect with him on LinkedIn or visit www.archerim.com.

Navigating the financial world can be complex, with an abundance of investment advice, often contradictory. To help you achieve your financial goals, here are ten golden rules that could lead to a better investment experience.

The stock market is driven by buyers and sellers setting prices through millions of trades daily. Trust in market pricing, which reflects the collective knowledge and analysis of Wall Street professionals. This approach helps you avoid trying to time the market, which is notoriously difficult and unreliable.

Long-term investment strategies are crucial. While some mutual funds may outperform the S&P 500 in the short term, this is rare over the long term. Even seasoned analysts can’t predict market movements consistently. Stick to your investment strategy and ignore short-term market noise to avoid potential losses.

On that same token, don’t make your investment decisions only based on past performance. Just because a mutual fund blew everyone away last year doesn’t mean it will thrive this year.

In general, investors who hold tight to a long-term perspective and stay committed to their investment philosophy will more likely see growth in their portfolio. History tells us that the markets have provided enough growth to beat inflation, so sit tight and let the market work for you.

Academic research has identified certain factors that may help you get the best return for your investments:

If you focus your portfolio toward these known factors, you may have a higher probability of better returns.

Diversification is essential, but don’t limit it to your own country. The U.S. represents only half of the global market capital. By diversifying internationally, you can access a wider array of investment opportunities, which is a key part of smart investment strategies.

Like rules #2 and #3, attempting to time the market is a risky endeavor. The stock market is unpredictable, and trying to forecast its movements can lead to unnecessary anxiety and potential losses. Focus on a globally diversified portfolio to benefit from opportunities wherever they arise.

Emotional investing can lead to poor decisions. Recognize your emotional triggers and maintain discipline. A financial advisor can provide objective investment advice and help you stay on track during market volatility.

Media often sensationalizes market movements, leading to unnecessary stress. Stick to your investment plan and avoid reacting to headlines. A disciplined approach is key to navigating the stock market successfully.

Since you can’t control the market no matter how hard you try, work on clarifying your goals and needs and work with an advisor to create a plan tailored to your unique situation.

Investing doesn’t have to be complicated, and it doesn’t have to scare you. If you want to pursue a better investment experience, implement these tips into your investment strategy and you may improve your chances of better investment returns and a secure financial future. At Archer Investment Management, we hold true to these ten rules and value disciplined, unemotional, and highly-diversified investing. You will receive objective advice from us as we work together to customize an investment plan for you. If you have any questions about these tips, click here to schedule a phone call. I’d love to hear from you!

About Richard

Richard Archer is a financial advisor and the President of Archer Investment Management with more than eighteen years of industry experience. Largely working with successful individuals and couples, he specializes in providing comprehensive investment guidance and personalized care and attention to each client. Along with holding a Bachelor of Science in Economics and a MBA, he is a CERTIFIED FINANCIAL PLANNER™ certificant and a Chartered Financial Analyst®. He combines his advanced industry education and knowledge with his genuine care for people to provide clients with an exceptional experience. To learn more about Richard, connect with him on LinkedIn or visit www.archerim.com.

George and I had been with an investment firm that promised many things they never got to deliver. We are so grateful to have found Archer Investments. Emily,Richard and all of the staff are extremely knowledgeable and so personal. We feel like family to them.We also feel so comfortable with our financial planning that has transpired, feeling confident in our long range plans, short term goals, the security of having ample insurance and medical coverage along with complete documents (POA’s, wills, healthcare POA’s, everything to make any transition smooth for our family). It is a tremendous relief to have everything in place. Their wealth of knowledge and attention to detail is impeccable. We feel so blessed to have found them and highly recommend their comprehensive services.

Andrea & George

Received via WealthTender: April 4, 2024

Working with Emily, Richard, and the team has been great! Their insight has been invaluable for me across a variety of domains. Their approach builds from goals backwards — we met together to outline short and long-term goals and then used those goals to create a plan across a variety of decisions, from home ownership to car insurance to investment and much more. Richard and Emily truly do a great job of drawing me into the loop, ensuring that the financial plan we develop reflects my goals and wishes. Before settling with Archer Investments, I talked with a number of other advisors and none of them had the combination of professionalism, attention to detail, and comprehensive services offered by Archer.

Ben

Received via WealthTender: July 1, 2024

I’m not finance-oriented by any measure, but luck came my way for once and I found myself having enough assets to need some help. Only I didn’t know what kind of help I needed and it’s easy to get overwhelmed quickly and I was on like year number whatever of being overwhelmed and I just kicked that can down the road every year. After a short search, I found Archer’s team and quickly just pushed other options off the table and signed on. They’ve actually been able to simplify things in a way that makes me feel like I can manage my life and not worry about it all for the first time in years. I basically had all eggs, but no basket. Now I have a comprehensive plan from some incredible staff and I actually love the process instead of dreading the matter. Simply put, Archer has changed how I view my own finances and what used to be a cause of stress for me is now a giant sigh of relief. I said in the title it was the best decision ever and I mean it: this has 100% seriously no-fingers-crossed changed my life. If you’re like me and you’ve been debating if you even need this kind of help, then yes… yes, you do!

Scott Eaton

Received via WealthTender: July 10, 2024