- Pre-IPO SpaceX planning starts with knowing exactly what you own, how concentrated you are, and what liquidity may or may not be available.

- The biggest risks usually involve taxes, timing, and having too much of your net worth tied to one company before an IPO or tender window opens.

- A strong plan should be built in stages, coordinated with the right advisors, and documented before emotions or tight deadlines drive decisions.

If SpaceX equity makes up a large portion of your net worth, pre‑IPO planning isn’t about optimizing returns, it’s about managing risk, taxes, and optionality before liquidity arrives.

This checklist reflects the most common issues we see among SpaceX employees as equity values grow and decisions become harder to reverse.

You don’t need to act on everything at once, but you do want to understand the full picture before a narrow liquidity window opens.

1. Inventory Your SpaceX Equity (Know What You Actually Own)

Before any strategy discussion, get clarity on the basics:

- Number of shares owned (vested vs unvested)

- Option types (ISOs, NSOs)

- Exercise dates and prices

- Cost basis and holding periods

- Transfer restrictions or consent requirements

- Exposure through prior tender offers or side vehicles

Many planning mistakes happen simply because this information isn’t centralized.

Talk to your financial advisor to understand how this applies to your personal situation.

2. Understand Your Concentration Risk

Ask yourself honestly:

- What percentage of my net worth is SpaceX equity?

- Is my income also tied to the company?

- Would a significant decline materially change my lifestyle or plans?

If your career, income, and investments all depend on the same company, concentration risk is likely higher than it feels day‑to‑day.

3. Model Multiple Liquidity Scenarios (Not Just the IPO)

Pre‑IPO planning shouldn’t assume one outcome.

- IPO sooner than expected

- IPO later than expected

- Partial liquidity via tender offers

- Extended private period

- Market‑driven valuation changes

Each scenario affects taxes, diversification timing, and risk exposure differently.

👉 Learn more about SpaceX IPO equity risk and taxes.

4. Review Tax Exposure Early (Before Decisions Are Forced)

Key questions to evaluate in advance:

- What is my estimated capital gains exposure at IPO pricing?

- How does AMT factor into my option history?

- Would staged diversification materially reduce tax impact?

- How does my state residency affect outcomes?

Tax strategies are far more effective before liquidity, not after.

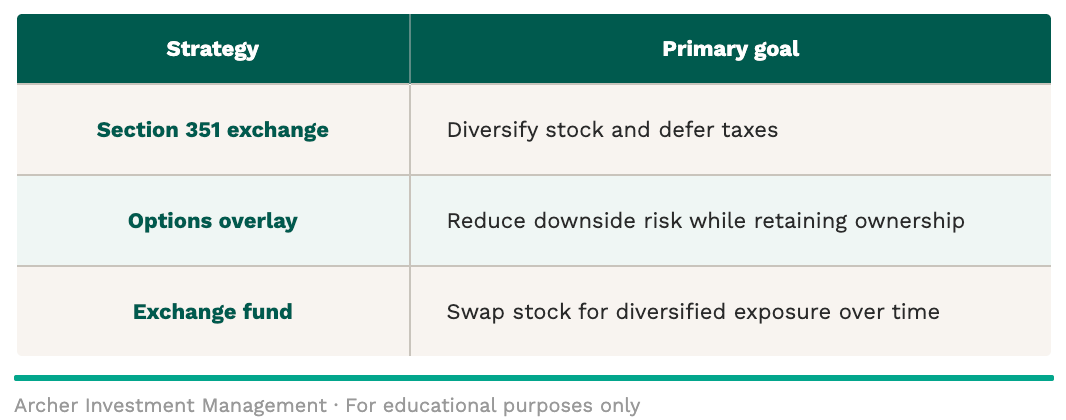

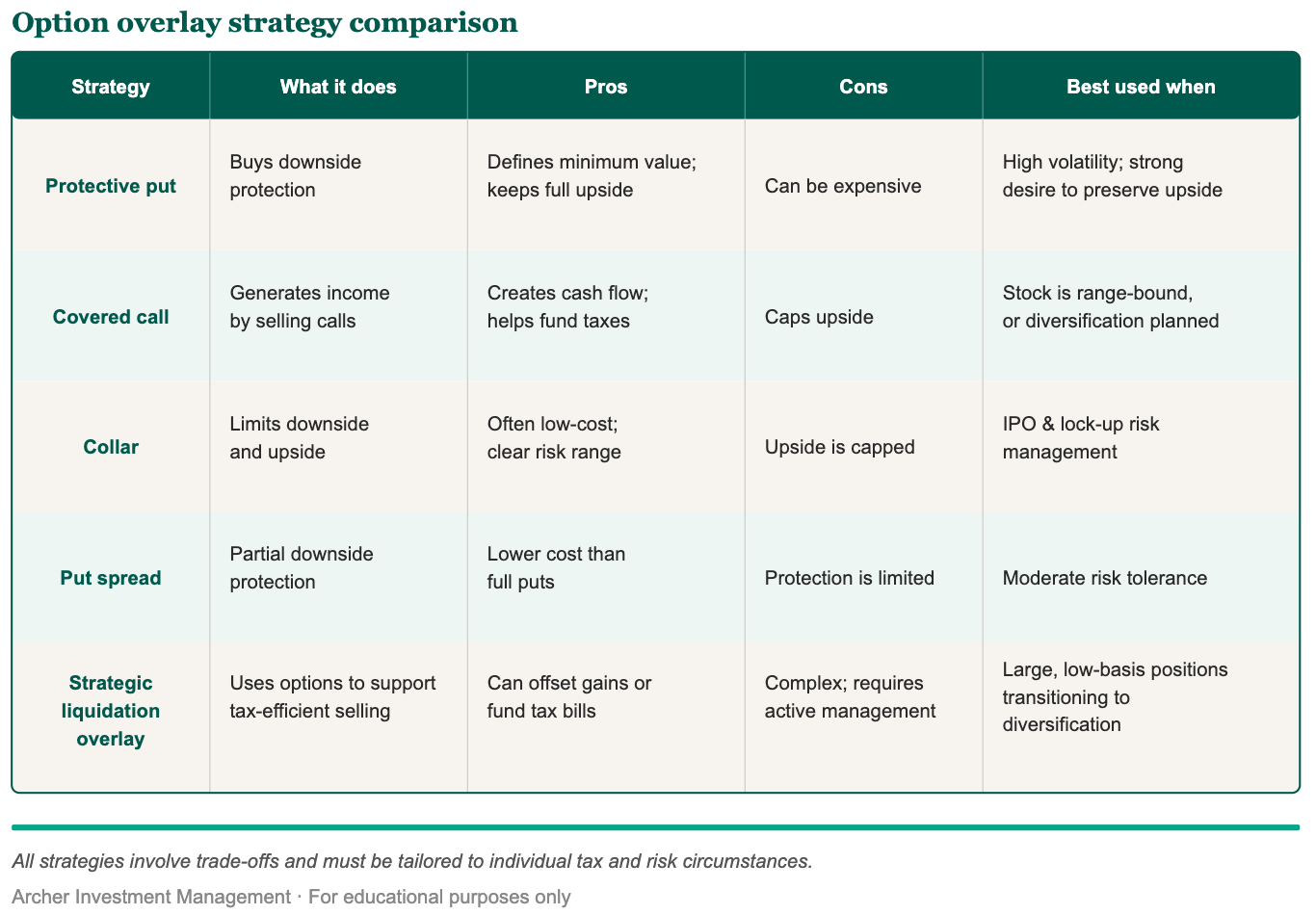

5. Evaluate Diversification Tools (and Their Trade‑Offs)

Common strategies to consider pre‑IPO:

- Holding a concentrated position for upside

- Options overlays to manage downside risk

- Section 351 exchanges for diversification with tax deferral

- Exchange funds with long lockups

- Charitable planning for highly appreciated shares

Each involves trade‑offs around control, liquidity, fees, and future taxes. There is no default “right” answer.

6. Stress‑Test Liquidity Needs

Ask:

- How much true liquidity do I need in the next 1–3 years?

- Do I have sufficient cash outside SpaceX equity?

- Are upcoming expenses (home, taxes, family, lifestyle) funded?

Illiquid wealth creates stress, even when headline net worth is high.

7. Revisit Risk Tolerance Honestly

Risk tolerance often changes as numbers get bigger.

- How would I feel if SpaceX represented 80%+ of my net worth at IPO?

- Would volatility affect decision‑making or sleep?

- Do I want certainty, flexibility, or maximum upside?

Planning should match behavior, not just math.

8. Coordinate Advisors Early

Pre‑IPO planning works well when advisors collaborate before decisions are locked in.

- Financial planner with equity‑comp expertise

- Tax advisor familiar with stock‑based compensation

- Legal counsel for transfer or fund structures

Misalignment between advisors often creates unnecessary cost and complexity.

9. Build a Staged Plan, Not a Single Bet

For most SpaceX employees, diversification works efficiently when approached in phases:

- Pre‑IPO risk management

- Initial liquidity event planning

- Tax‑aware diversification over time

- Post‑IPO portfolio construction

Optionality is often more valuable than precision.

10. Document the Plan (So Emotions Don’t Drive Decisions)

Finally:

- Write down your assumptions

- Define thresholds for action

- Set expectations before emotions are involved

- Revisit and update annually

When liquidity arrives, decisions may happen fast. The plan should already exist.

Final Thought

Being pre‑IPO at SpaceX is exciting—but it creates complexity many tech professionals rarely face.

Thoughtful planning ahead of liquidity can help you make more informed decisions, maintain flexibility, and reduce the risk of rushed choices. Regardless of when or how SpaceX ultimately goes public.

Our team of CERTIFIED FINANCIAL PLANNER® professionals (serving clients nationwide, virtually) works with SpaceX employees to help them understand their equity, explore their options, and build personalized financial plans around what matters most to them.

If a large portion of your net worth is tied to SpaceX stock, a thoughtful plan can help you think more clearly about taxes, liquidity, concentration risk, and what this wealth is meant to do for your life.

Book a call to build a thoughtful plan for your SpaceX equity, so you can worry less about money and focus more on the life you are building.

This article is for general educational purposes only and is not individualized tax, legal, or investment advice. Tax rules are complex and can change, and outcomes depend on your specific situation. You should consult your CPA and/or attorney regarding your circumstances. Archer Investment Management is an SEC-registered investment adviser; registration does not imply a certain level of skill or training. Investing involves risk, including the possible loss of principal.

What the Tax Picture Could Look Like

What the Tax Picture Could Look Like The State-Tax Swing: Why Residency Matters in SpaceX IPO Planning

The State-Tax Swing: Why Residency Matters in SpaceX IPO Planning

IPO Wealth Is a Life-Planning Moment

IPO Wealth Is a Life-Planning Moment