Understanding Qualifying and Disqualifying Dispositions for ISOs: A Complete Guide

Key Takeaways:

- Selling your ISO shares too early (i.e. a disqualifying disposition) can very well mean that you’ll end up paying more taxes than if you had waited for a qualifying sale.

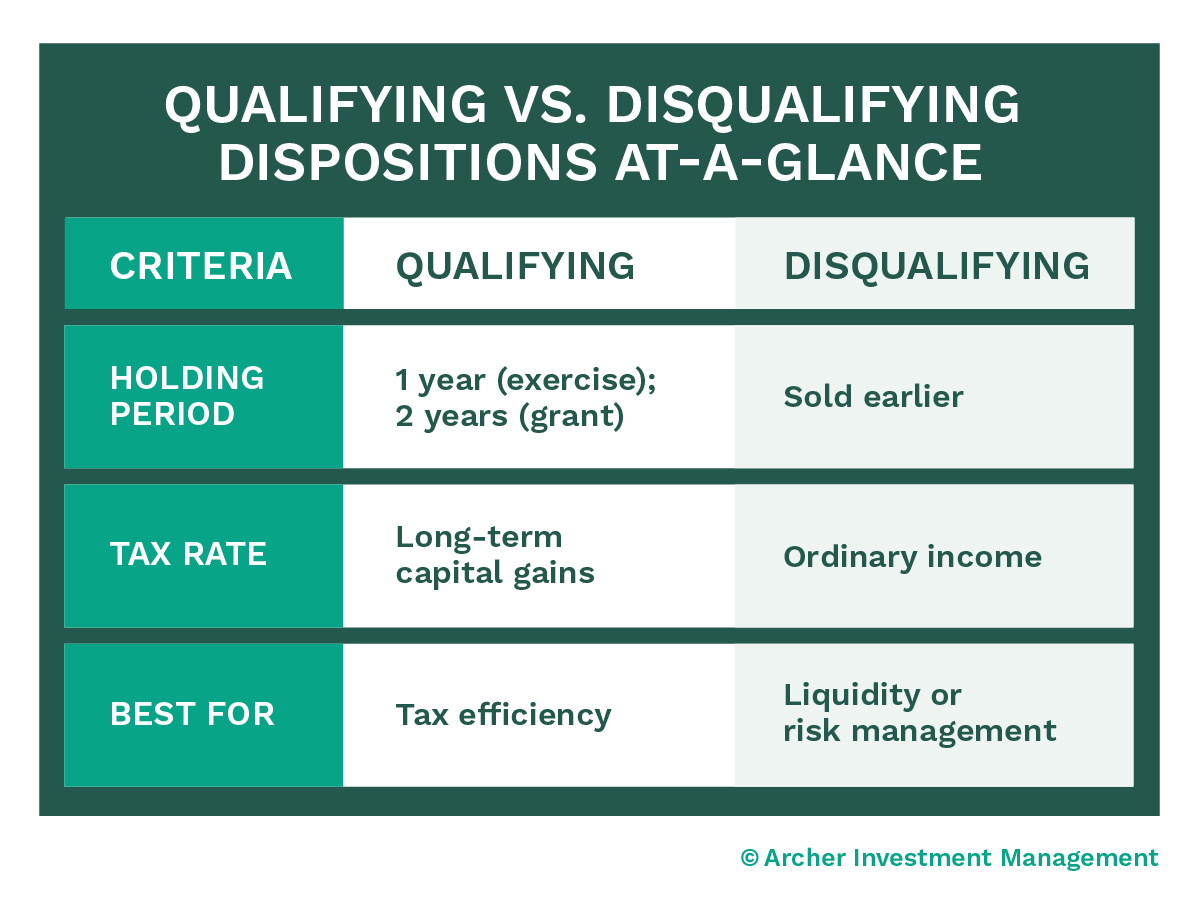

- Timing matters: hold your shares for at least 1 year after exercise and 2 years after the grant date to get lower long-term capital gains tax rates.

- Sometimes, selling early still makes sense if you need cash or just want to reduce risk (for example, if your company’s future feels uncertain).

An Important Decision: Should I take a Qualifying Disposition or Sell Earlier, Triggering a Disqualifying Disposition?

If you’re a tech professional who has received Incentive Stock Options (ISOs) from your employer, one of the biggest financial decisions you’ll make is deciding when to sell your shares after you’ve purchased them (a step known as exercising).

Exercising ISOs presents a critical decision: Should you aim for a qualifying disposition or selling earlier, triggering a disqualifying disposition? The choice isn’t just about taxes; it can play a role in your financial goals, such as buying a home or managing risks in your portfolio.

What Are Qualifying and Disqualifying Dispositions?

Qualifying Disposition

A qualifying disposition happens when you sell your ISO shares after meeting two specific holding period requirements:

1. At least one year after the exercise date (when you purchased the shares)

2. At least two years after the grant date (when you received the options)

When you meet both of these requirements, you’ll pay the lower long-term capital gains tax rate (0%, 15%, or 20%, depending on your income) instead of the much higher ordinary income tax rates.

Watch Out! Many people only focus on the one-year holding period after exercise. But don’t forget—you also need to hold them for at least two years after the grant date. Missing this second requirement could mean paying much higher taxes by triggering a disqualifying disposition.

Disqualifying Disposition

A disqualifying disposition happens if you sell your ISO shares too early—before meeting the two holding periods.

When this happens, your profits are taxed at ordinary income tax rates, which can go as high as 37% for top earners. That’s a big difference from the lower rates when the sale is considered a qualifying disposition.

Viewing ISOs and Employer Shares from a Portfolio Perspective

It’s exciting to hold stock in your company, but holding too much can be risky. If the stock price drops, your portfolio could take a big hit.

That’s why it’s important to think about your ISOs as part of a bigger picture and make sure your investments are well-balanced to protect your long-term financial health.

The Real Tax Impact: Why It Matters

The difference between qualifying and disqualifying dispositions has a big impact on how much of your profit you get to keep after taxes.

Here’s the breakdown:

-

- Qualifying Disposition: You’ll pay the lower long-term capital gains rate (around 15-20% for most people).

-

- Disqualifying Disposition: You’ll pay the higher ordinary income tax rate, which can reach up to 37%.

Let’s say you’re in the highest tax bracket. The difference between these rates could mean paying 17% more in taxes—potentially costing you tens of thousands of dollars, depending on how much stock you’re selling.

Struggling to untangle the best time to sell your stock? That’s exactly what we help our clients with every day. Schedule a call with us, and we can help you figure it out.

When a Disqualifying Disposition Might Make Sense

Even though disqualifying dispositions can come with higher taxes, there are times when they make good financial sense.

If you have immediate liquidity needs—whether for buying a house, paying for an emergency, covering education costs, or any other major expense—having money on hand might be more valuable than holding out for tax savings.

Selling early can also help reduce your financial risk.

For example, if you’re worried about your company’s performance, stock market swings, or your own job security, it could be smarter to sell some shares now and diversify your investments rather than waiting just to save on taxes.

Here’s a real-life example:

One of our clients, a Tesla employee, faced an unexpected layoff. They needed money quickly to relocate, buy a bigger home, purchase a second car, and prepare for a baby.

In this situation, selling the shares immediately—even with the higher tax hit—was the right move.

The immediate funds allowed them to meet their needs without unnecessary stress.

Understanding the Alternative Minimum Tax (AMT)

Let’s talk about the Alternative Minimum Tax (AMT), which can complicate ISO decisions.

If you exercise your ISOs but don’t sell the shares right away, you might owe AMT even though you haven’t made any money from selling them.

Here’s how it works: The IRS looks at the “paper gain”—the difference between the price you paid to exercise your options and the market value of the stock. Even if you’re just holding the shares, this paper gain can create a tax bill. It’s one more thing to factor in when planning your ISO strategy.

A paper gain is like potential profit. It’s the difference between what you paid for your stock when you exercised your options and what the stock is worth today.

Even though you haven’t sold the stock or made any real money, the IRS looks at this potential profit and might tax you on it with the Alternative Minimum Tax (AMT). It’s like being taxed on money you don’t actually have in your pocket yet!

(We often refer to this potential profit as “an “unrealized” gain).

Five Key Considerations for Deciding When to Sell Your ISO Shares

There’s no one-size-fits-all answer for when to sell your ISO shares—it all depends on your personal situation and financial planning needs.

-

- Start by looking at your income level. If you’re in a higher tax bracket, the tax difference between qualifying and disqualifying dispositions becomes even more important.

-

- Next, think about market risk. Waiting to meet the waiting requirements for a qualifying disposition might save on taxes, but it also means holding onto your shares longer. If the stock price drops during the holding period, those tax savings could disappear.

-

- To stay on top of things, make sure you keep track of key dates such as your grant date, exercise date, and vesting schedules. Knowing these details can help you plan your sales effectively.

-

- A great strategy to lower risk is “staged selling.” Instead of selling all your shares at once, sell in smaller amounts over time. This approach balances market risk with tax benefits.

-

- Lastly, check how much of your portfolio is tied up in employer stock. Too much can leave you overexposed if your company’s stock takes a hit. Diversifying your investments is key to long-term financial stability.

Remember, tax laws aren’t set in stone

Tax laws change, which could affect how you plan your ISO sales. Changes to capital gains tax rates or AMT rules might also impact your strategy.

Staying informed about these potential shifts by working with a CERTIFIED FINANCIAL PLANNER® is important so you can adapt your plan and avoid surprises.

Next Steps

To make informed ISO decisions, take a close look at your grant dates and exercise dates, calculating the tax impact of a qualifying versus selling early to trigger a disqualifying disposition, and consider any immediate liquidity needs. Your risk tolerance also shapes your approach.

Once you have a clear sense of your financial picture, set a timeline for exercising and selling your shares based on the current market and your company’s performance.

Working with a CERTIFIED FINANCIAL PLANNER® experienced in equity compensation can help align your ISO strategy with broader financial goals, while a tax professional can provide tailored advice for your situation.

The Bottom Line

Qualifying dispositions can be a great way to save on taxes, but they’re not always the right choice. The best decision balances tax savings with your personal needs and financial goals.

Sometimes, it’s worth paying a little more in taxes if it helps you meet a big life goal, reduce risk, or feel more financially secure.

Need help developing a custom ISO strategy?

Reach out to our team at Archer Investment Management to schedule a consultation.

We specialize in helping tech professionals make smart, confident decisions about their equity compensation.

Schedule a call with our team.

Editor’s Note: This article was originally published on August 15th, 2022. It has been updated to offer an expanded scope of the subject area.

Read More On Equity Comp From Our Team: