The coronavirus-driven recession and uncertainty will make retiring in Austin within the next 5 years challenging. The record volatility, recent legislation, and economic disruption mean that the decisions you make next will define your retirement. Create confidence in your plan for a work-free life by downloading this free checklist. Worried about what’s going on and want advice now? I save a few appointments each week — grab one by calling 800-840-5946.

Austin retirees and those facing retirement soon, the pandemic and economic crisis mean historic levels of uncertainty. To learn how to retire comfortably in uncertain times, please download this FREE guide. Need advice now? I save a few appointments each week — grab one by visiting https://archerim.com/call.

IN FINANCE AND IN LIFE, EXPECTATIONS OFTEN ECLIPSE REALITY.

They become anchors for how we evaluate opportunities (like companies and stocks) and our own sense of happiness.1

They also make us fixate on what could or should have been, not what’s right in front of us.1

When reality doesn’t line up with our expectations, unhappiness, resentment, and anxiety usually follow.2

These negative feelings can intensify when we sense uncertainty.3 We get anxious about our hopes, goals, and dreams for the future when we feel like everything’s unpredictable.4

Yet, it’s not impossible to be happy when life throws us a curveball and the future seems uncertain.

When we’re grateful, we can let go of our expectations. That can lead to greater happiness and life satisfaction, no matter how uncertain the present is—or the future may be.5

HOW TO BE MORE GRATEFUL & HAPPIER: 6 QUESTIONS

1. WHAT IS A MAGICAL MEMORY YOU HAVE FROM THE LAST FEW MONTHS?

We instinctively focus more on the negative than the positive. When times are tough, we expect the worst. To see things in a more positive light, we have to consciously set aside the negativity.6

Recalling happy memories is a quick way to do that. Even remembering a simple act of kindness can make you feel happier.7

2. HOW HAS YOUR PERSPECTIVE CHANGED OVER THE LAST FEW MONTHS?

Consider the interactions, experiences, or people who have changed the way you think about something recently. Think about what you’ve learned.

Change and uncertainty can test our strength and character. How we stand up to the challenge may not just change our perspectives. It can also keep us grounded and spark personal growth.8

3. WHAT DO YOU TAKE FOR GRANTED?

It’s natural to take things for granted as we get used to them, even if they matter a lot to us. If we don’t take time to appreciate them while we have them, though, we may never get the chance.

Writer Robert Brault may have said it best with this: “Enjoy the little things in life because one day you’ll look back and realize they were the big things.”

4. WHAT DO YOU WANT TO REMEMBER FROM THIS PERIOD OF YOUR LIFE?

“We do not remember days; we remember moments.” These words from Cesare Pavese ring true if you’re in your 20s, your 90s, or anywhere in between.

Whether you’re starting your career, raising kids, or enjoying retirement, recognize the good moments that are shaping this phase of your life. If you do, you’ll enjoy them far more as they’re happening.

5. WHAT EXPERIENCES HAVE YOU HAD THAT YOU’RE GRATEFUL FOR?

Some experiences create memories that last a lifetime. Family dinners, vacations, celebrations, major life milestones, and once-in-a-lifetime moments can shape us forever and for the better.9

They can also have positive impacts on the way we learn, see the world, and respond to unknown situations in the future.10

6. WHAT DO YOU FEEL LUCKY TO HAVE THAT SOME OTHERS DO NOT?

This doesn’t have to be extravagant. It can be simple, like some treasured part of your day or week.

It can also be unique and intangible, like a relationship you have with a friend, sibling, child, or spouse. In fact, these close relationships are the key to fulfillment and long-term happiness. Appreciating how special they are can help you make them stronger while bringing you more satisfaction.11

Risk Disclosures: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. The S&P 500 is an unmanaged composite index considered to be representative of the U.S. stock market in general. All index returns exclude reinvested dividends and interest. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. For illustrative purposes only.

Risk Disclosure: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability, or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. These are the views of Finance Insights and not necessarily those of the named representative or firm, and should not be construed as investment advice.

But we don’t live in a perfect world. Far from it.

That means our emotions impact our financial choices more than we realize.1

Shockingly as much as 95% of our purchase choices are made subconsciously, driven by our emotions—as little as 5% are based in logic (and that’s when we’re in a good headspace and feeling comfortable and secure).2

When we’re faced with uncertainty, fear and instinct can take over and push logic right out of the window.3

Ironically, these instincts often make things worse. Emotional reactions can lead to poor choices and the losses you were trying to avoid in the first place.5

The best way to avoid letting your hardwired biases take over? Use these strategies. They can help you fare better in any crisis. They may even make you a savvier investor.

Click Here for full article and to sign up for our Visual Insights Newsletter!

With many people in Austin facing job losses or furloughs, the CARES Act provides additional flexibility for accessing retirement accounts. However, it’s crucial to consider various factors before deciding how to handle an old 401(k) or employer plan.

This FREE guide is designed to assist investors in managing an uncertain situation by outlining the available options for an old employer plan. Feeling overwhelmed and need personal advice right away? Call 800-840-5946 for a complimentary 1-on-1 phone appointment to discuss your 401k withdrawal strategy and money management concerns.

This FREE Guide reveals the 5 options to revive your old zombie plans!

In a perfect world, logic would always guide our financial decisions. Emotions wouldn’t come into play.

But we don’t live in a perfect world. Far from it.

That means our emotions impact our financial choices more than we realize.1

Shockingly as much as 95% of our purchase choices are made subconsciously, driven by our emotions—as little as 5% are based in logic (and that’s when we’re in a good head-space and feeling comfortable and secure).2

When we’re faced with uncertainty, fear and instinct can take over and push logic right out of the window.3

Your brain will make you want to react quickly to protect yourself and avoid the pain you anticipate from potential losses.4

Ironically, these instincts often make things worse. Emotional reactions can lead to poor choices and the losses you were trying to avoid in the first place.5

The best way to avoid letting your hardwired biases take over? Use these strategies. They can help you fare better in any crisis. They may even make you a savvier investor.

6 SECRETS TO MAKE YOU A SMARTER INVESTOR

1. AVOID THE OVERCONFIDENCE TRAP

Overconfidence is a killer. In fact, research shows that the more experience you have as an investor, the more overconfident you tend to be.6

Stay realistic and grounded by a strategy. Get advice before making big decisions.

2. FORCE EMOTIONS INTO THE BACKSEAT

Losing money hurts. The truth is that the pain of losses can actually be more intense than any satisfaction from gains. Economists call that “loss aversion.”7 The pressure of anxiety or uncertainty can lead to irrational choices that actually work against our big-picture financial goals.

Don’t give into fear or panic when they show up. Focus on logic and rely on your professional for guidance.

3. FRAME PERFORMANCE IN A MORE MEANINGFUL WAY

Framing is everything when it comes to evaluating performance. That’s because the way information and events are presented to us can sway our perception and influence our decisions.8

Look beyond short-term outcomes when framing performance. Think about your longer-term goals and the progress you are making towards them, even when short-term corrections slow your progress.

4. NEUTRALIZE YOUR RECENCY BIAS

Recent events usually influence you more than those in the distant past. Why? The human brain remembers recent events more clearly and gives them outsized weight when making decisions. Your brain can mislead you by expecting more of what you’ve seen already. And that can lead to overconfidence and emotional decisions.9

Resist this tendency by remembering the market is constantly changing. Over the long term, bear markets recover. And no bull market lasts forever.

5. CONSIDER MULTIPLE PERSPECTIVES

With decision making, it’s natural to focus on one aspect or one piece of information as a starting point. Often, that can greatly influence your final choice. This is known as “anchoring bias,” which can give you tunnel vision. It can lead you to fixate on a single data point, like an investment’s price, while ignoring other key information.

To fight it, seek out more information. Think critically about multiple perspectives, and don’t forget to consider future potential.

6. SLOW DOWN & TAKE TIME TO THINK MORE DEEPLY

Humans like to make snap decisions. And, when you’re stressed out, you’re far more likely to make impulsive decisions. The problem is that “gut” decisions are made based on instinct, habit, and emotions, instead of logic and facts. When you’re in gut-decision mode, it can be much harder to make goal-oriented choices.10

Take your time when making financial decisions and let your brain shift into analytical mode. With a little time, emotions cool down, and you’ll typically consider more alternatives.11

We can’t foresee or control downturns or upswings. We can only control our mindset, our emotions, and our financial choices.

FINANCIAL LESSON: KEEP YOUR COOL & FOCUS ON THE LONG GAME WHEN CRISIS STRIKES

Markets and economies are never predictable or under our control. We can’t foresee or control downturns or upswings. We can only control our mindset, our emotions, and our financial choices.

That’s easy to lose sight of during periods of economic uncertainty and financial stress.

But, if you can focus on the long game and improve your mental game, you’ll come out stronger and more prepared.

That can make you less vulnerable to hardwired human biases and help you make better financial decisions, no matter what the markets are doing.

As a financial adviser, one of my most important jobs is to help you become a smarter, more capable investor. That involves using psychology and behavioral finance to help you learn more about how your brain works and improve your financial behaviors.

I’m also here to be an objective accountability partner. I talk my clients through emotional decisions, and I can be an important voice of reason and calm when markets are turbulent and it feels like the sky is falling.

If you’re curious about behavioral finance—or if you need a sounding board for a financial decision—I’m here for you. Don’t hesitate to call me at 800-840-5946.

I’d be happy to answer your questions and share some more advice.

Risk Disclosures: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. The S&P 500 is an unmanaged composite index considered to be representative of the U.S. stock market in general. All index returns exclude reinvested dividends and interest. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. For illustrative purposes only.

Risk Disclosure: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability, or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. These are the views of Finance Insights and not necessarily those of the named representative or firm, and should not be construed as investment advice.

“If you aim at nothing, you will hit it every time.” – Zig Ziglar

That’s true for most aspects of life, including our finances. Understanding the importance of financial goal setting can be crucial to success. Most of us realize that. It’s why we set New Year’s resolutions—and why more than half of all Americans set some type of financial goal as a resolution each year.1

As great as financial goal setting is, it won’t accomplish much for you if you can’t achieve them. And, maybe not so surprisingly, the vast majority of people (92% according to the research) don’t achieve their goals.2

The Challenge of Financial Goal Setting

Why do we (and I’m including myself here) struggle so much to meet the goals we set for ourselves? Is it because we don’t want to? Because we lack commitment? Not so much.

One big reason behind our failures is that most of us lack a clear connection between our present reality and the future we’d like to achieve. That vagueness can cut the emotional ties to a financial goal, draining the passion and commitment that actually lie within us.3 When we don’t connect to our goals at a deep level, it’s easy to get off track and lose our momentum. This is especially true for long term financial goals, which require sustained effort over time.

So, how can we stay on track to achieve our financial goals?

By reconnecting with the vivid emotions behind them and digging deeper to uncover our inner passions and motivations behind our goals.3 A simple way to dig deeper into the underlying reason for your financial goals is by peeling back the layers and asking yourself “why?” three times. This approach is particularly effective when aiming to meet your long term financial goals.

Unlock the Passion Inside Your Financial Goals by Asking These 3 Whys

1st “WHY”: Peel back the first layer

Start by asking yourself why you have set a specific financial goal: “Why do I want to (obtain this financial goal)?” Financial goals to earn more, save more, or build wealth are usually linked to a deeper desire, like the desire to have more time, more freedom, or an early retirement.

Answer this first question to help reveal the general motivation behind your financial goal. Financial goal setting is not just about numbers; it’s about the purpose behind those numbers.

Still Not There Yet? Keep Asking “Why.”

People are like onions. Sometimes, you have to peel back more layers to uncover the clear vision behind your goals. When you’re able to dig deep and connect your financial goals to your innermost desires, you’ll stay excited about them for the long run. This approach is especially helpful when setting long term financial goals, as it keeps you motivated through the years.

Financial Lesson: Uncovering Your Passion Can Be the Best Motivation for Achieving Your Financial Goals

For most people, financial goal setting takes time to achieve. From spending less to saving more, these goals take consistent effort and action. They can require you to change your habits, make sacrifices, and stay the course for years.

And that’s hard.

But it can be a lot easier if you’re able to stay connected to the “why” and the passion behind your goals. This is particularly important for long term financial goals, which might feel distant or abstract without a strong emotional connection.

Maybe you want more free time so you can enjoy special experiences with your family because you’ve missed important occasions before. Maybe you’re focused on creating a lasting foundation for your children because your family struggled while you were growing up. Perhaps you dream of owning a vacation home where your family can gather because you have fond memories of family gatherings in the past.

Why?

Because, if you’re truly passionate about your financial goals, you’ll stay excited about them for the long run. And that can mean you’ll be far more likely to work harder toward achieving your goals and you’ll be far less likely to give up on them.4

Adapting Your Financial Goals Over Time

Of course, the financial goals you set today can change over time. With age and changing life circumstances, new financial goals can replace the ones you set 5, 10, or even 20 years ago. No matter when or why those goals may change, staying connected to the “why” behind them can go a long way to helping you achieve them. This flexibility is key in successful financial goal setting, especially as it relates to long term financial goals.

If you’re thinking about the “why” behind your financial goals and want to talk about them, give my office a call at 800-840-5946.

I’d love to hear more about your goals, why you chose them, and where you are at in your journey toward achieving them. I have a lot of experience helping my clients with their financial goals, and I look forward to the opportunity to help you, too.

Richard Archer, CFA, CFP®, MBAArcher Investment Management

Risk Disclosures: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. The S&P 500 is an unmanaged composite index considered to be representative of the U.S. stock market in general. All index returns exclude reinvested dividends and interest. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. For illustrative purposes only.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability, or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. These are the views of Finance Insights and not necessarily those of the named representative or firm, and should not be construed as investment advice.

Life has changed; how do we adapt without losing sight of what we want to achieve?

As you’ve heard me say before, no one knows how the future will play out, but we should still look ahead and think through the consequences of what’s happening. (More about this kind of second-order thinking ahead.)

I believe that our society and our economy are experiencing a massive paradigm shift.

We will never go back to the world we had before COVID-19, and the lens that we used to evaluate ideas, markets, economies, and personal choices over the last decade may not be sufficient for the next decade.

Here are just a few things that I see changing as a result of what’s going on now:

Social Support: 36.5 million Americans have become unemployed in two months, and the effects are rippling through families, communities, and the economy.1 The government has responded with trillions of stimulus dollars to individuals and businesses. More relief is likely to come. What does this mean for our society? Who should get a helping hand in tough times? Will we permanently expand the social safety net?

Work: Thrown into the largest work-from-home experiment in history, more workers and employers will transition to remote work post-pandemic. This shift in work has major implications. Which places will be a draw if workers can live anywhere and employers can have their pick of a nationwide (or global) workforce? Will those who must physically show up demand different compensation?

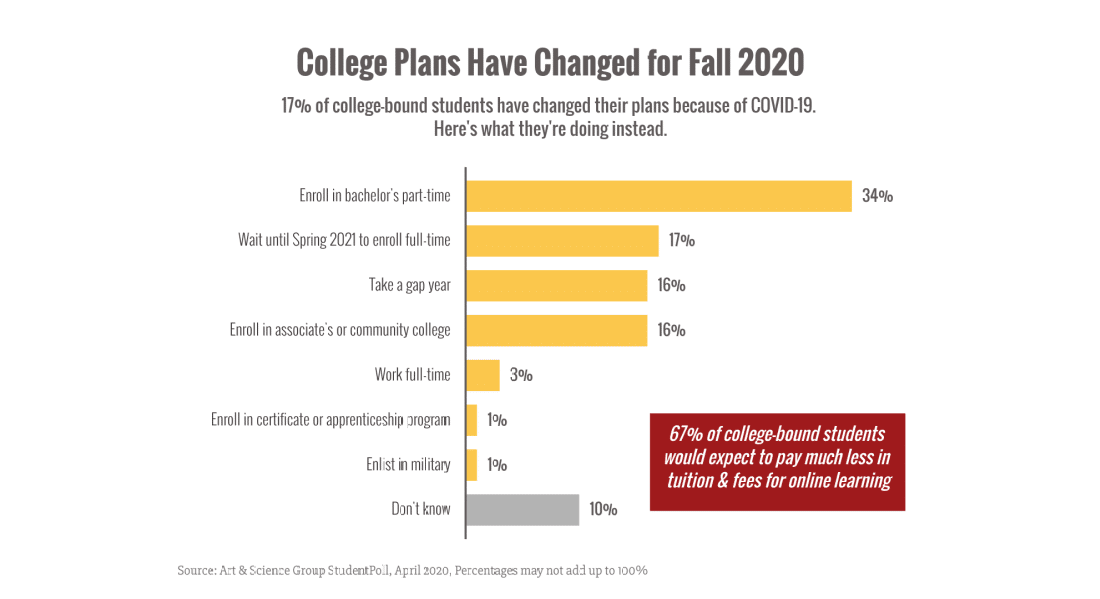

Education: Students, parents, schools, and universities are being forced to re-evaluate the definition of education (and its price tag) now that the on-campus experience has gone online. What’s missing if you attend from home? How much should education cost? What alternatives to a traditional four-year degree will arise?

Shopping & Entertainment: Brick-and-mortar retailers may never recover from the body blow dealt by pandemic lock-downs. Online shopping, grocery delivery, and digital services may finally overtake offline channels. What will the retail landscape look like when it’s easier (and maybe safer) to eat, shop, and watch at home?

No one has all the answers about the new world and things are not always what they seem.

Though it appears that the stock market has moved past the pandemic, we shouldn’t celebrate just yet.

Why?

Much has changed in the world and we’re still playing out first-order effects. More consequences are coming.

“What are the second- and third-order consequences of this?” is a question big thinkers like Ray Dalio (Manager of the largest hedge fund in the world) ask about complex scenarios.

Here’s what they mean:

First-order thinking is fast and simple: B is the logical outcome of event A.

But then what? What happens as a consequence of B?

And what happens as a result of that? And what is the follow-on effect of that?

Second-order thinking is about interactions and complex systems. It’s slow and hard (but mastering it can put us steps ahead of the crowd).

Understanding the new world that’s growing out of the pandemic requires thinking through these higher-order consequences and developing a new lens to navigate the uncertain waters ahead.

How can we adapt? How can we still pursue our goals in a totally different world?

We think it through with humility and an open mind.

We hone our second-order thinking skills by asking: what could happen? And then what? How likely is it that I’m right? What could happen if I’m wrong? How do I position myself?

We’ll do it together.

COVID-19 is going to be with us for the rest of 2020 and possibly into 2021. So we’re adapting.

At Archer Investment Management, it means we will continue to hold virtual client meetings for the foreseeable future. We are happy to reopen our office once we know more.

It also means big changes in our personal lives. Many of our children will be attending school online through the end of the school year and maybe even this fall.

Our anticipated summer vacation to Disney Magic Kingdom is canceled, but we’re hoping to spend time on Lake Austin instead.

We’re taking it day by day and thinking through those higher-order effects.

How about you? What changes are you making to your plans this summer and fall?

P.S. A number of clients and friends have reached out to talk through options around a potential lay-off, buy-out offer, or early retirement. If this is on your mind, please let me know. We can work through it together.

P.P.S If you’ve got a kid in college this fall, I have a question for you: is virtual university still a compelling offer? Are you and your student considering a gap year or some alternative? Please let me know. I’m interested in learning from your experience.

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Risk Disclosures: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. The S&P 500 is an unmanaged composite index considered to be representative of the U.S. stock market in general. All index returns exclude reinvested dividends and interest. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. For illustrative purposes only.

It’s been weeks since we shuttered the office and started working from home and, like many, I’m feeling the strain of upended life.

How about you? Are you ready to venture out again? Are you dying to go to the beach like me?

In this article, I thought I’d give you a rundown of some of the latest economic projections, as well as a sneak peek of what post-lockdown life could look like for us soon.

(Ready for a break from COVID-19? No worries. Scroll down to the P.S. for some wonderful distractions.)

On to the economy.

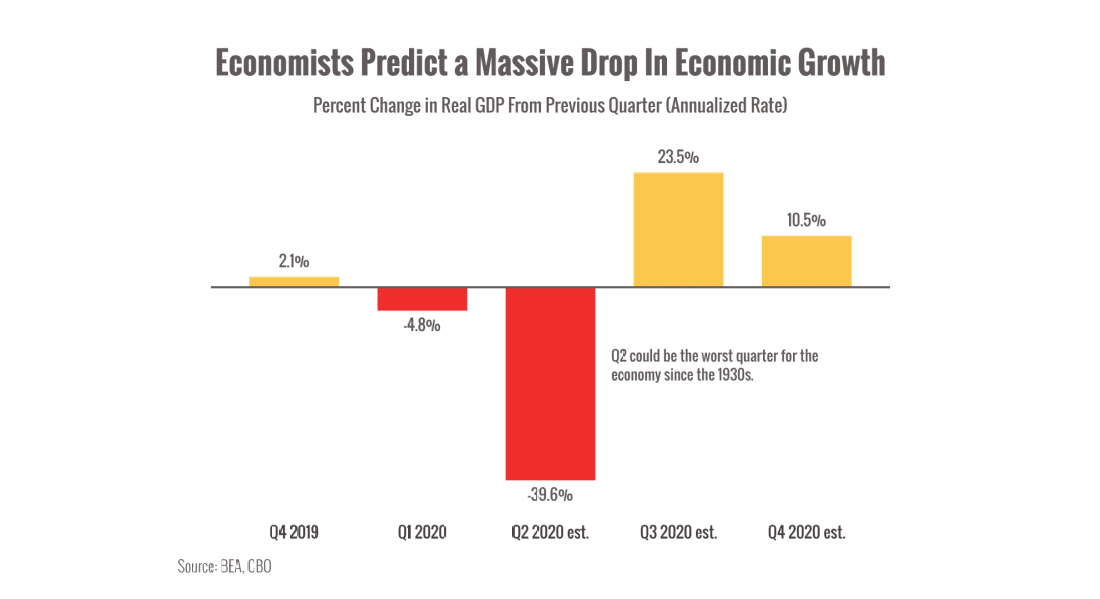

You may have seen a headline showing that U.S. economic growth dropped -4.8% in the first quarter after posting 2.1% growth in Q4 2019. That’s not a surprise.1

Unfortunately, worse news is ahead since widespread layoffs and shutdowns didn’t hit until late March. Here’s a projection of what the next few quarters could look like for the economy.2

You can see in this chart that the coronavirus hit the economy like a tsunami. Q2 could be the worst quarter since the Great Depression.3

The arithmetic of recovering from a 30%+ drop in economic growth means that it could take many months (maybe even years) to return to pre-pandemic GDP levels, especially if we face multiple waves of infection.

Let’s mentally prepare for that.

April 2020 is likely to be one of the worst months for the economy in history; contradictorily, it was also a blockbuster month for stocks.4

Why are stocks so disconnected from the economic data?

Fundamentally, a stock’s price is an attempt to put a value on the underlying company’s earnings now and in the future. Complicating the calculation are factors like fear, greed, uncertainty, and movements in the overall market.

While economic data looks back at what has already happened (or is happening now), the stock market looks forward at the trajectory of the business environment. Framed that way, the rally isn’t so unusual since investors are expecting things to get better, not worse.

Will the rally continue? Hard to say. Volatility is very likely to be the name of the game for months.

Economists are predicting a rebound in Q3 2020. Are they right?

You know by now that we can’t perfectly predict what the recovery will look like; all economic estimates are based on educated guesses about spending, business investment, trade, and other factors. The biggest unknown is “personal consumption” by folks like you and me. Our spending drives 70% of economic growth.

The pace of the recovery depends on how quickly businesses reopen and consumers go out to shop, eat, travel, and spend money. If people don’t feel safe going out or don’t feel confident enough to open their wallets, growth could take longer to come back.

What could life look like as Texas reopens? While America is just now taking the first tentative steps toward reopening, many countries around the world are farther along, offering us a glimpse of what daily life might look like in a world where the coronavirus still remains a threat.5

Hong Kong: Restaurants are open but tables must be spaced farther apart.

South Korea: Pro sports are back but athletes play to empty stadiums. Temperature screening is in place in many buildings.

Taiwan: Schools are in session but assemblies are canceled and students wear face masks in class.

Australia: Beaches are open but sunbathing, picnicking, and large gatherings are verboten.

How long will coronavirus precautions overshadow our daily life? Realistically, some restrictions are likely to drag on until a vaccine or breakthrough treatment becomes widely available.

What do you think? What will our “new normal” look like?

P.S. I promised you some distractions from the coronavirus, and here they are:

Watch jellyfish float at the Monterey Bay Aquarium (includes relaxing music!).

Dream of a Caribbean vacation with the beach cam at the Soggy Dollar Bar on Jost Van Dyke.

SCUBA dive vicariously in a kelp forest off Anacapa Island.

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Risk Disclosures: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. The S&P 500 is an unmanaged composite index considered to be representative of the U.S. stock market in general. All index returns exclude reinvested dividends and interest. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. For illustrative purposes only.

Are we past the peak? Or just over the first summit of a mountain range?

Are we safe yet?

After weeks of restrictions, it’s easy to feel that we’re swirling in a maelstrom of uncertainty, helpless to make decisions when so much remains unknown and out of our control.

I think that’s normal. We’ve traded a trip on the highway for an off-roading adventure. And we don’t know where it’s going to take us this year.

So let’s lean into the uncertainty. Let’s embrace it and use it to explore and appreciate what really matters.

Our health. Our family, friends, and loved ones. Our home. Our community. Our compassion and creativity. Our resilience as human beings.

As for me, I have some moments of frustration, but I’m staying grounded by learning to cook.

I’m learning a lot about myself. I’ve learned that I might be pretty good at creating sauces. I’ve learned that I’m very bad at making pizza crusts, but I’m humbly trying to get better. Did you know there are more than thirty different ways to bake them and one method even uses a waffle maker?

I’m working on gratitude and enjoying simple things like playing catch with Annie and finally watching the two new Star Trek series.

I’m grateful to have a wonderful home and meaningful work.

I’m grateful to have you.

On the professional side, I’m focused on what I can control on my clients’ behalf and staying abreast of what might come next. My mantra right now is: “one day at a time.”

How are you? I’d love to hear how you are coping. What lessons are you learning about yourself? What have you had the courage to try for the first time? Hit “reply” and let me know.

This pandemic is scary. But it’s also a once-in-a-lifetime chance to hit the “reset” button and connect with the creativity, joy, and good old human ingenuity that can flourish within the limitations of pandemic life.

Eventually, we’ll recover from the coronavirus. It’s not clear yet what that will look like, and we’ll likely see more hard days before we get there. Businesses will reopen, people will go back to work, the recession will pass, and the country will rebuild.

We will heal. But some marks will remain as reminders of our experience.

The Great Depression taught people to clip coupons and “make do or go without.” 9/11 upended our travel rituals and awareness of terrorism.

Some lessons from the pandemic will stay with us long after the immediate crisis fades. Some will be unconscious; maybe we’ll become a society of dutiful hand washers and social distancers.

Others will be lessons we consciously take with us about our values and ability to adapt to circumstances far beyond our control.

I’m hopeful and excited to see what we learn. Let’s make it good.

How has the crisis changed your perspective? What new values and priorities will you bring out of your experiences?

P.S. Do you know someone who is having a hard time and could use some financial advice? I’m holding a few spots open for folks who could use a professional’s help. If you can think of someone, please call 800-840-5946 to let me know.

Risk Disclosures: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results. The S&P 500 is an unmanaged composite index considered to be representative of the U.S. stock market in general. All index returns exclude reinvested dividends and interest. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. For illustrative purposes only.

Get Financial Tips, Insights, and Resources delivered to your inbox

We honestly could not ask for a better partner.

My husband and I have been working with Richard and the team at Archer Management Group for over 10 years, and we honestly couldn’t ask for a better partner. Richard is not only incredibly knowledgeable — he’s also just a genuinely great person. We always feel like he’s looking out for us and helping guide us in the right direction. He’s helped us through an inheritance, purchasing homes, managing complex stock options/RSAs at work and helps keep our finances running smoothly.

The whole team is super responsive and on top of things, and they’ve made the whole process of managing our finances feel less stressful and more secure. We really trust Richard with our money, and that peace of mind is huge for us. I highly recommend Richard and team!

Dave

Received on Google July 2025

These testimonials were provided by current Archer Investment Management clients and may not be representative of the experiences of other clients. The clients were not compensated, nor are there material conflicts of interest that would affect the given testimonials. You can view a complete list of reviews at Emily Rassam’s and Richard Archer’s Wealthtender profiles.

Most thorough and personable financial planners and wealth managers

George and I had been with an investment firm that promised many things they never got to deliver. We are so grateful to have found Archer Investments. Emily,Richard and all of the staff are extremely knowledgeable and so personal. We feel like family to them.We also feel so comfortable with our financial planning that has transpired, feeling confident in our long range plans, short term goals, the security of having ample insurance and medical coverage along with complete documents (POA’s, wills, healthcare POA’s, everything to make any transition smooth for our family). It is a tremendous relief to have everything in place. Their wealth of knowledge and attention to detail is impeccable. We feel so blessed to have found them and highly recommend their comprehensive services.

Andrea & George

Received via WealthTender: April 4, 2024

Comprehensive financial planning

Working with Emily, Richard, and the team has been great! Their insight has been invaluable for me across a variety of domains. Their approach builds from goals backwards — we met together to outline short and long-term goals and then used those goals to create a plan across a variety of decisions, from home ownership to car insurance to investment and much more. Richard and Emily truly do a great job of drawing me into the loop, ensuring that the financial plan we develop reflects my goals and wishes. Before settling with Archer Investments, I talked with a number of other advisors and none of them had the combination of professionalism, attention to detail, and comprehensive services offered by Archer.

Ben

Received via WealthTender: July 1, 2024

I was quite literally afraid of getting help and of all that it involved. It’s been wonderful. No kidding: best decision ever!

I’m not finance-oriented by any measure, but luck came my way for once and I found myself having enough assets to need some help. Only I didn’t know what kind of help I needed and it’s easy to get overwhelmed quickly and I was on like year number whatever of being overwhelmed and I just kicked that can down the road every year. After a short search, I found Archer’s team and quickly just pushed other options off the table and signed on. They’ve actually been able to simplify things in a way that makes me feel like I can manage my life and not worry about it all for the first time in years. I basically had all eggs, but no basket. Now I have a comprehensive plan from some incredible staff and I actually love the process instead of dreading the matter. Simply put, Archer has changed how I view my own finances and what used to be a cause of stress for me is now a giant sigh of relief. I said in the title it was the best decision ever and I mean it: this has 100% seriously no-fingers-crossed changed my life. If you’re like me and you’ve been debating if you even need this kind of help, then yes… yes, you do!

Scott Eaton

Received via WealthTender: July 10, 2024

We honestly could not ask for a better partner.

My husband and I have been working with Richard and the team at Archer Management Group for over 10 years, and we honestly couldn’t ask for a better partner. Richard is not only incredibly knowledgeable — he’s also just a genuinely great person. We always feel like he’s looking out for us and helping guide us in the right direction. He’s helped us through an inheritance, purchasing homes, managing complex stock options/RSAs at work and helps keep our finances running smoothly.

The whole team is super responsive and on top of things, and they’ve made the whole process of managing our finances feel less stressful and more secure. We really trust Richard with our money, and that peace of mind is huge for us. I highly recommend Richard and team!

Dave

Received on Google July 2025

×

Their expertise in the tech startup industry is invaluable to navigate company stock options and instill confidence when exercising.

Working with Emily, Richard, and the rest of the Archer team has been an absolute game-changer for my financial well-being. From our very first meeting, their friendliness and professionalism put me completely at ease. I feel like they genuinely care about my goals, and they’ve been incredibly patient in answering all my (many!) questions. If you are anything like me starting this process with no idea what the heck your financial goals are, don’t worry, they will gently guide you. They do a thorough intake process over several meetings to identify goals, risk tolerance, and get to know clients.

I had a scattered mess of accounts due to changing employers and random investments over the years. Now all of those accounts are organized and manageable from a single place. Their expertise in the tech startup industry is invaluable to navigate company stock options and instill confidence when exercising. What truly sets them apart is their high quality tooling. I love love love that they have everything in a secure cloud with custom dashboards, and all signatures are electronic – no more printing and mailing, thank goodness! They also pre-fill any necessary forms with my personal info which is a huge timesaver. Their responsiveness is truly remarkable; I’ve always received incredibly fast replies. This level of dedication is rare and greatly appreciated. Last but not least, I get to sit back and watch my investments grow. For the first time in my life, I can see a path to early retirement.

I wholeheartedly recommend Archer Investment Management to anyone seeking a trustworthy, knowledgeable, and highly responsive financial planning service.

Maggie

Received on Google May 2025

×

Personalized to our lifestyle

Richard and Emily are a fantastic team! We reached a point in our life that we thankfully had options for our money, investments, and the way we wanted to live our lives. Their approach is personalized to understand your relationship with finances and tailored to how you want to enjoy your money now and into the future. We had considered ourselves smart with our finances, but the Archer team exceeded our expectations and opened up several opportunities to maximize our potential. We got support & recommendations for exactly how to allocate, invest, and yes spend our money the way we wanted our lifestyle to be. This approach gave us the peace of mind knowing our future was secure, our 3 kids college was within reach, and our “fun” spending on family and vacations was a balanced way for us to enjoy the long journey. And on top of that, they make the process simple and as easy as possible. So glad we found this team.

Danny and Julia

Received on WealthTender October 2024

×

I was quite literally afraid of getting help and all that it involved. It’s been wonderful. No kidding: best decision ever!

I’m not finance-oriented by any measure, but luck came my way for once and I found myself having enough assets to need some help. Only I didn’t know what kind of help I needed and it’s easy to get overwhelmed quickly and I was on like year number whatever of being overwhelmed and I just kicked that can down the road every year. After a short search, I found Archer’s team and quickly just pushed other options off the table and signed on. They’ve actually been able to simplify things in a way that makes me feel like I can manage my life and not worry about it all for the first time in years. I basically had all eggs, but no basket. Now I have a comprehensive plan from some incredible staff and I actually love the process instead of dreading the matter. Simply put, Archer has changed how I view my own finances and what used to be a cause of stress for me is now a giant sigh of relief. I said in the title it was the best decision ever and I mean it: this has 100% seriously no-fingers-crossed changed my life. If you’re like me and you’ve been debating if you even need this kind of help, then yes… yes, you do!

Scott

Received on WealthTender July 2024

×

Most thorough and personable financial planners and wealth managers.

George and I had been with an investment firm that promised many things they never got to deliver. We are so grateful to have found Archer Investments. Emily,Richard and all of the staff are extremely knowledgeable and so personal. We feel like family to them.We also feel so comfortable with our financial planning that has transpired, feeling confident in our long range plans, short term goals, the security of having ample insurance and medical coverage along with complete documents (POA’s, wills, healthcare POA’s, everything to make any transition smooth for our family). It is a tremendous relief to have everything in place. Their wealth of knowledge and attention to detail is impeccable. We feel so blessed to have found them and highly recommend their comprehensive services.

Andrea and George

Received on WealthTender 2024

×

We’ll forever remember Emily as the person who said we could retire.

We’ve worked with Emily for a few years now, and have been so impressed. She is a wealth of knowledge and a way of being able to answer a lay person’s questions in a very thorough and understandable manner. She can answer any question you throw at her with detail and clarity. She is honest, credible and trustworthy. She is very knowledgeable about the technology she has available to use and is able to provide strong visuals and projections to help with making decisions. She is always willing to meet and discuss a given topic or to provide an update on our portfolio. We’ll forever remember Emily as the person who said we could retire. That’s a hard decision to make and she was able to clearly show us the path. I’d highly recommend Emily to work with as a Financial Advisor.

Kay

Received on WealthTender June 2022

×

There is no one else I would trust with my financial future. This advisor/client relationship is the best I’ve ever had.

Emily has been a lifesaver for me in so many ways. I needed a Financial Advisor that I could trust, and I could not be more pleased. She is honest, provides great advice, guidance and always goes the extra mile for her clients. She is always professional, knows what is going on in the industry and what services the company offers I could benefit from. I retired at the end of 2018, but before I did, I met with Emily, and we went over what my retirement would look like. There is no one else I would trust with my financial future. This advisor/client relationship is the best I’ve ever had. She keeps me on the right road! I appreciate her so much.

Elaine

Received on WealthTender June 2022

×

The entire experience has brought us a great sense of security

My wife and I have been with the Archer team for almost 3 years. Throughout, they have been responsive, thorough, and professional. All of the staff are excellent communicators, in person or via email/texts! The entire experience has brought us a great sense of security – from the initial “get to know you” conversations, with Rich doing an excellent job of listening, to the mid-course corrections when life changes. Initially they brought great organization to our portfolio, and our retirement is organized and easy to track. Whenever it’s time for us to do some homework, they are great at helping us with our end of the tasks.

Karen

Received on WealthTender February 2023

×

Before meeting with the Archer Team, we had concerns about the value wealth management would bring to the table. Those concerns were quickly squashed after meeting with the team.

We have really enjoyed working with Archer Investment Management. We reached out to them because we wanted financial guidance and reassurance as we move toward reaching education goals for our children and retirement goals for ourselves. We knew we needed to diversify some of our assets but had no idea how to do so in a financially savvy way. Before meeting with the Archer Team, we had concerns about the value wealth management would bring to the table. Those concerns were quickly squashed after meeting with the team. They pointed out things we hadn’t thought of and questions we hadn’t asked ourselves to help create more specific goals than we would have set for ourselves. They kindly and patiently walked us through creating a plan that fit our comfort level and helped us take the steps needed to put that plan in action. If any of this sounds overwhelming, I can’t reiterate enough how much patience and support we received. It never felt overwhelming. We are so relieved to now have the support of these specific experts to help us stay on track to hitting our goals.