When You Should or Should Not Max Out Your 401(k)

At Archer Investment Management, we help tech professionals and pre-retirees gain clarity and confidence about their financial futures — so they can worry less about money and focus more on enjoying the life they’ve worked hard to build.

Many of our clients are high earners navigating tech equity compensation, IPO windfalls, and high-stress roles, or individuals preparing for retirement who want a smooth and confident transition.

What makes us unique as financial advisors is our belief that money isn’t just math — it’s deeply connected to your decisions, your dreams, and sometimes even your worries.

That’s why we design financial plans that don’t just prepare you for the future, but also make your life feel better today.

By weaving together financial planning, tax strategies, and investment management with proactive guidance, we help clients replace stress and second-guessing with clarity, confidence, and more room for the things that matter most.

The result is a clear plan that reduces stress and creates flexibility in your financial life.

Whether you’re aiming to retire early, shift into more fulfilling work, or maximize the wealth you’ve worked so hard to build.

Here’s what clients say about working with Archer:

“I was quite literally afraid of getting help and of all that it involved. It’s been wonderful. No kidding: best decision ever!

I’m not finance-oriented by any measure, but luck came my way for once and I found myself having enough assets to need some help. Only I didn’t know what kind of help I needed and it’s easy to get overwhelmed quickly and I was on like year number whatever of being overwhelmed and I just kicked that can down the road every year.After a short search, I found Archer’s team and quickly just pushed other options off the table and signed on. They’ve actually been able to simplify things in a way that makes me feel like I can manage my life and not worry about it all for the first time in years. I basically had all eggs, but no basket. Now I have a comprehensive plan from some incredible staff and I actually love the process instead of dreading the matter.

Simply put, Archer has changed how I view my own finances and what used to be a cause of stress for me is now a giant sigh of relief. I said in the title it was the best decision ever and I mean it: this has 100% seriously no-fingers-crossed changed my life. If you’re like me and you’ve been debating if you even need this kind of help, then yes… yes, you do!”

Scott

Received via WealthTender on July 10, 2024

Disclosure: These testimonials were provided by current Archer Investment Management clients and may not be representative of the experiences of other clients. The clients were not compensated, nor are there material conflicts of interest that would affect the given testimonials. View more reviews on WealthTender or Google.

That said, we know we aren’t the right fit for everyone. That’s why we’ve compiled this list of other respected financial advisors in Austin for 2026 to help you find the right match for your unique situation.

Disclaimer: This list is not exhaustive. It reflects our opinion only and should not be considered a testimonial or endorsement of any advisor included.

Specialty:

Why They Stand Out: LeafHouse is one of Austin’s largest independent RIAs, managing over $2 billion in assets. They’re known for their retirement plan investment management expertise, fiduciary advice, and proprietary technology platform that streamlines complex portfolio oversight.

Specialty:

Why They Stand Out: Reap operates as a “virtual family office,” guiding clients through tax strategy, estate planning, retirement income, and investments. They’re particularly strong for entrepreneurs and affluent families who want to preserve and grow wealth across generations.

“Chris and his team enabled me to retire and continue to enjoy a very comfortable lifestyle. Their level of professionalism, fiscal knowledge and integrity is very hard to find in these competitive times. Reap Financial guided us through the many investment loopholes, ensuring we placed our savings in the right buckets.

For anyone looking for financial peace of mind in their later years, I would not hesitate to recommend Chris and his team at Reap Financial.”

Keith M.

Received via Google Review in May 2025

Specialty:

Why They Stand Out: Austin Wealth emphasizes collaboration and education. Clients gain access to a secure wealth management system to track progress, paired with regular check-ins and proactive communication.

Specialty:

Why They Stand Out: Led by Dr. Massi de Santis, Ph.D. and CFP®, DESMO integrates behavioral economics into comprehensive, fee-only planning. Their approach helps clients identify and overcome biases that can derail financial progress.

Specialty:

Why They Stand Out: Founded by Jane Mepham, CFP®, Elgon focuses on immigrant families and professionals navigating equity compensation. Jane’s IT background and personal immigrant experience give her unique insight into the challenges these clients face.

“Jane is not only a great financial advisor but also knowledgeable, kind, and hard working.

She’s ready to do the research to help advise on tricky financial decisions or provide the depth of knowledge she already has on cross-border financial advice.

We’re so happy we chose Jane as our advisor.”

Mat B.

Received via Wealthtender in March 2025

When you’re searching for the right financial advisor, it can be difficult to spot the differences.

Here’s what sets Archer apart:

Archer Investment Management has been recognized with several national awards, including:

To learn more about our professional certifications and awards, click here.

See all award disclosures here.

Austin is home to a wide range of excellent financial advisors, each with unique specialties and strengths. If you’re looking for guidance, you have strong options across the city.

But if you’re a tech professional navigating equity compensation or a pre-retiree preparing for your next chapter, Archer Investment Management may be a great fit for you.

We help clients reduce stress, create flexibility, and build an intentional financial plan that supports the life they want to live today and tomorrow.

Want to learn more? Schedule a free consultation with one of our CERTIFIED FINANCIAL PLANNERS® today.

Key Takeaways:

Incorporating restricted stock and RSUs (restricted stock units) into your financial plan can get complicated. You will need to make plenty of decisions, such as how long you will hold your shares if you should sell them and put them into an alternative investment, or if you will use the money to meet one of your financial goals.

If your head is spinning, take heart. Here are 10 simple tips to help you maximize your restricted stock and RSUs.

Restricted stock units (RSUs) are a form of equity compensation that companies grant to employees, in which the employees receive company shares upon completion of a specified vesting schedule. Think of them as a bonus – paid in stock shares instead of cash.

They differ from stock options in that employees do not have to purchase shares at a particular stock price; rather, they are given shares outright once they vest.

By contrast, “restricted stock” is actual stock granted on the award date, but it generally cannot be sold or transferred until it vests. Because you technically own restricted stock at grant (although with restrictions), it may be eligible for dividends and potentially an 83(b) election.

RSUs and restricted stock tie employee interests to the company’s future performance.

However, if you’re not sure how to fit either of these into your overall financial plan, the following rules should help guide you in determining an ideal approach.

In order to make quality decisions, you need to determine what you hope your stock will do for you.

When you eventually sell the shares, where do you want that money to go? How do your shares and their potential sale fit in relation to your other income, 401(k), and other savings?

When setting your objectives, keep both your timelines and your financial goals in mind. Whether you have restricted stock or RSUs, these awards can help fund key financial priorities, such as:

By outlining these aims at the outset, you’ll be able to make more informed choices about whether to hold, sell, or reinvest your shares.

You should also consider how RSUs fit into your broader compensation, especially if they represent a large portion of your earning potential. Be sure to keep them on your radar alongside salary, bonuses, and any other benefits you receive.

It is important to know the dates your grants will vest since you will need to pay taxes on the resulting income.

If you want to avoid a hefty tax bill, it requires planning ahead. Your vesting schedule will depend on your company and the conditions they place on the stock, but it is usually time-based, requiring you to work at the company for a certain period before vesting can occur.

One helpful approach is to create a timeline or calendar event marking each vest date. By planning around these dates, you’ll have a clearer picture of how your income may spike during certain periods, potentially moving you into a higher tax bracket.

You might also want to see if your company offers any flexibility in your vesting; for instance, some companies allow for acceleration of vesting in certain circumstances, such as mergers, acquisitions, upon disability, or retirement eligibility.

Either way, thinking ahead helps with tax planning and allows you to anticipate your tax liability (the amount you’ll need to pay the government when tax time comes) long before you owe it.

📝 Note: Tax liability is a fancy word for the amount of money you owe in taxes to the government.

If you leave your company before your restricted stock vests, you will usually forfeit the unvested grants.

There can be exceptions to this, so be sure to gather all the details from your company before you make the decision to leave.

If you have a significant amount of shares that haven’t vested, it might be worth it to stay with your company long enough to benefit from this reward for your service.

Evaluate the current and future value of your RSUs or restricted stock and think about whether staying at the company until a certain vest date could be financially advantageous. If you are planning a career change, weigh the opportunity cost of leaving unvested RSUs behind against the benefits of a new role.

Sometimes, negotiations with a new employer could include a ‘make-whole’ RSU or stock grant to compensate you for the value you are giving up.

Your taxable income will be the market value of the shares at vesting and is subject to federal income tax, Social Security, and Medicare, plus any state and local income tax.

📝 Note: Taxable income is the part of your income that the government uses to figure out how much tax you owe.

Your company may offer you a few ways to pay taxes at vesting, such as withholding shares for taxes, a sell-to-cover transaction for taxes of a portion of the shares, a salary deduction, or simply a check payment. A 22% standard supplement tax withholding, as a sale from shares vested is fairly common. The standard withholding rate often becomes 37% if your total income exceeds $1,000,000.

When you eventually sell the shares, you will pay capital gains tax on any appreciation the stock has from the vest date until the sale date.

To further minimize your overall tax liability, consider increasing contributions to tax-deferred accounts—such as 401(k)s, Health Savings Accounts (HSAs), or other qualified plans—during your vesting years. By carefully coordinating these strategies, you can maintain more control over your income and keep your total tax liability in check.

With restricted stock (not RSUs), you have the option to make a Section 83(b) election with the IRS within 30 days of the grant date.

An 83(b) election allows you to pay taxes on the value of the stock at the grant date rather than the vesting date.

If you believe the stock price will be higher on the vesting date and you are confident you will meet vesting requirements, this can be a beneficial move for you.

Also, moving the time of taxation to the grant date starts the capital gains holding period earlier, which can make a difference at the eventual sale of the shares.

However, keep in mind that making an 83(b) election does involve certain risks: if the stock doesn’t appreciate or—worse—loses value, you might have paid more taxes upfront than necessary. Additionally, if you leave the company or fail to meet vesting requirements, you generally cannot get a refund on taxes already paid because the election is irrevocable once filed. It’s important to consult with a tax advisor or financial planner to confirm if an 83(b) election aligns with your overall financial goals and risk tolerance.

Be sure to anticipate what restricted stock and RSUs will do to your tax rates when you vest.

The extra income could push your income into a higher tax bracket, raise your rate of capital gains tax, and trigger extra Medicare taxes, possibly costing you thousands of dollars. If you plan ahead, you can implement strategies that could keep you in the lower tax brackets.

When you hold restricted stock or RSUs, it’s important to understand their impact on both ordinary income and capital gains taxes.

Tax rates vary by state—some impose high income and capital gains taxes, while others charge little or none. Your location can significantly influence what you owe. Other factors, such as your total income, the length of time you have held the shares, and your filing status, also play a role.

Typically, the market value of your shares becomes taxable income when they vest, which may increase your federal and state tax burden. (Remember, if you made a Section 83(b) election for restricted stock, the income would have been taxed earlier.)

After vesting, any additional increase in the share price is usually treated as capital gains.

Selling shares within a year of vesting usually means paying short-term capital gains taxes at ordinary income tax rates (currently 10% to 37% federally).

Wait over a year, and you’ll generally qualify for long-term capital gains rates (currently 0% to 20% federally). Plus an additional 3.8% net investment income tax for those individuals with high income.

Please note: Tax laws and rates can change, and states may have unique rules that affect your final bill. To stay informed, it’s wise to keep track of any changes or work with a financial professional.

Whether or not you sell your shares at vesting will depend on multiple factors, such as tax planning, financial planning goals, and company restrictions.

Your decision may be influenced by your cash needs, upcoming life events, and other financial planning factors, including diversification, dividends paid on your stock, and alternative investments.

If your company is publicly traded, there can be blackout dates that prevent you from trading and stock ownership guidelines that require you to keep a certain amount of stock. With private companies, there are probably restrictions in your grant or SEC rules that will impact when you can sell.

Even though you can’t transfer or sell restricted stock until it vests, the stock is still issued to you and in your name, which means you could receive dividends.

If you have unvested RSUs, this does not apply.

But when a company pays dividends on outstanding shares of stock, it can choose to pay dividend equivalents on RSUs. These may be deferred or accrued to additional units and then settled when the unit vests.

It’s a cliché, but when it comes to your portfolio, you don’t want to keep all of your eggs in one basket. You don’t want too much of your net worth tied up in your company stock, and since restricted stock and RSUs vest over time, it’s easy to miscalculate how much of your portfolio is reliant on the success of your company.

In order to avoid overconcentration, consider working with a CERTIFIED FINANCIAL PLANNER® to determine how much your holdings in company stock contribute to your overall net worth.

A financial advisor can help you tackle concentration risk by building a plan to gradually reduce your holdings in company stock.

Together, you might set up automatic sales when shares vest, look for opportunities to offset gains through tax strategies, or use hedging tools to manage volatility.

The proceeds can then be channeled into a well-diversified blend of broad-market funds, bonds, or alternative investments, reducing your reliance on a single stock’s performance. Ongoing reviews help make sure your approach stays in step with your goals, risk tolerance, and changes in the market.

With a more diversified approach, you won’t be betting your financial future on a single stock. And as life changes, regular check-ins will help you stay on track.

Managing restricted stock, RSUs, and everything that comes with them can get complicated fast. From taxes to timing to investment decisions, there’s a lot to think about — and it’s easy to feel unsure about the best path forward.

That’s where we come in.

At Archer Investment Management, we help tech professionals navigate the ins and outs of equity compensation and build plans that align with their lives and goals.

If you have ESOs, restricted stock, or RSUs, don’t hesitate to reach out to us to help you maximize restricted stock units (RSUs) and incorporate them into your overall financial picture.

If you’re looking for clarity and a strategy that ties it all together and takes the guesswork out of managing your restricted stock, we’re here to help.

Click here to schedule a call and let’s talk.

If you enjoyed this article, you may also like these:

Key Takeaways:

If you’ve received Incentive Stock Options (ISOs) from your employer, one of the biggest financial decisions you’ll make is deciding when to sell your shares after you’ve purchased them (a step known as exercising).

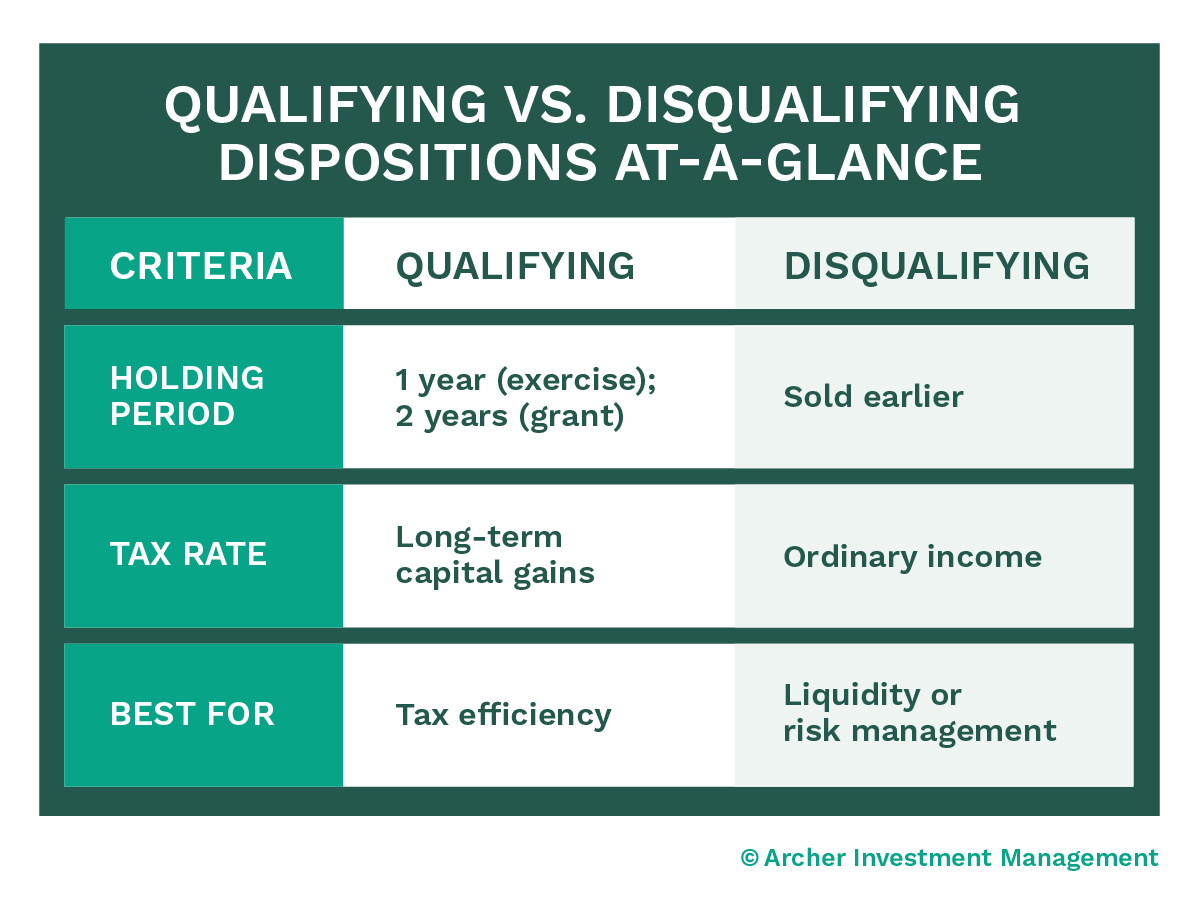

Exercising ISOs presents a critical decision: Should you aim for a qualifying disposition or selling earlier, triggering a disqualifying disposition? The choice isn’t just about taxes; it can play a role in your financial goals, such as buying a home or managing risks in your portfolio.

A qualifying disposition happens when you sell your ISO shares after meeting two specific holding period requirements:

1. At least one year after the exercise date (when you purchased the shares)

2. At least two years after the grant date (when you received the options)

When you meet both of these requirements, you’ll pay the lower long-term capital gains tax rate (0%, 15%, or 20%, depending on your income) instead of the much higher ordinary income tax rates.

Watch Out! Many people only focus on the one-year holding period after exercise. But don’t forget—you also need to hold them for at least two years after the grant date. Missing this second requirement could mean paying much higher taxes by triggering a disqualifying disposition.

A disqualifying disposition happens if you sell your ISO shares too early—before meeting the two holding periods.

When this happens, your profits are taxed at ordinary income tax rates, which can go as high as 37% for top earners. That’s a big difference from the lower rates when the sale is considered a qualifying disposition.

It’s exciting to hold stock in your company, but holding too much can be risky. If the stock price drops, your portfolio could take a big hit.

That’s why it’s important to think about your ISOs as part of a bigger picture and make sure your investments are well-balanced to protect your long-term financial health.

The difference between qualifying and disqualifying dispositions has a big impact on how much of your profit you get to keep after taxes.

Here’s the breakdown:

Let’s say you’re in the highest tax bracket. The difference between these rates could mean paying 17% more in taxes—potentially costing you tens of thousands of dollars, depending on how much stock you’re selling.

Struggling to untangle the best time to sell your stock? That’s exactly what we help our clients with every day. Schedule a call with us, and we can help you figure it out.

Even though disqualifying dispositions can come with higher taxes, there are times when they make good financial sense.

If you have immediate liquidity needs—whether for buying a house, paying for an emergency, covering education costs, or any other major expense—having money on hand might be more valuable than holding out for tax savings.

Selling early can also help reduce your financial risk.

For example, if you’re worried about your company’s performance, stock market swings, or your own job security, it could be smarter to sell some shares now and diversify your investments rather than waiting just to save on taxes.

Here’s a real-life example:

One of our clients, a Tesla employee, faced an unexpected layoff. They needed money quickly to relocate, buy a bigger home, purchase a second car, and prepare for a baby.

In this situation, selling the shares immediately—even with the higher tax hit—was the right move.

The immediate funds allowed them to meet their needs without unnecessary stress.

Let’s talk about the Alternative Minimum Tax (AMT), which can complicate ISO decisions.

If you exercise your ISOs but don’t sell the shares right away, you might owe AMT even though you haven’t made any money from selling them.

Here’s how it works: The IRS looks at the “paper gain”—the difference between the price you paid to exercise your options and the market value of the stock. Even if you’re just holding the shares, this paper gain can create a tax bill. It’s one more thing to factor in when planning your ISO strategy.

A paper gain is like potential profit. It’s the difference between what you paid for your stock when you exercised your options and what the stock is worth today.

Even though you haven’t sold the stock or made any real money, the IRS looks at this potential profit and might tax you on it with the Alternative Minimum Tax (AMT). It’s like being taxed on money you don’t actually have in your pocket yet!

(We often refer to this potential profit as “an “unrealized” gain).

There’s no one-size-fits-all answer for when to sell your ISO shares—it all depends on your personal situation and financial planning needs.

Remember, tax laws aren’t set in stone

Tax laws change, which could affect how you plan your ISO sales. Changes to capital gains tax rates or AMT rules might also impact your strategy.

Staying informed about these potential shifts by working with a CERTIFIED FINANCIAL PLANNER® is important so you can adapt your plan and avoid surprises.

To make informed ISO decisions, take a close look at your grant dates and exercise dates, calculating the tax impact of a qualifying versus selling early to trigger a disqualifying disposition, and consider any immediate liquidity needs. Your risk tolerance also shapes your approach.

Once you have a clear sense of your financial picture, set a timeline for exercising and selling your shares based on the current market and your company’s performance.

Working with a CERTIFIED FINANCIAL PLANNER® experienced in equity compensation can help align your ISO strategy with broader financial goals, while a tax professional can provide tailored advice for your situation.

Qualifying dispositions can be a great way to save on taxes, but they’re not always the right choice. The best decision balances tax savings with your personal needs and financial goals.

Sometimes, it’s worth paying a little more in taxes if it helps you meet a big life goal, reduce risk, or feel more financially secure.

Reach out to our team at Archer Investment Management to schedule a consultation.

We specialize in helping tech professionals make smart, confident decisions about their equity compensation.

Schedule a call with our team.

Editor’s Note: This article was originally published on August 15th, 2022. It has been updated to offer an expanded scope of the subject area.

Read More On Equity Comp From Our Team:

George and I had been with an investment firm that promised many things they never got to deliver. We are so grateful to have found Archer Investments. Emily,Richard and all of the staff are extremely knowledgeable and so personal. We feel like family to them.We also feel so comfortable with our financial planning that has transpired, feeling confident in our long range plans, short term goals, the security of having ample insurance and medical coverage along with complete documents (POA’s, wills, healthcare POA’s, everything to make any transition smooth for our family). It is a tremendous relief to have everything in place. Their wealth of knowledge and attention to detail is impeccable. We feel so blessed to have found them and highly recommend their comprehensive services.

Andrea & George

Received via WealthTender: April 4, 2024

Working with Emily, Richard, and the team has been great! Their insight has been invaluable for me across a variety of domains. Their approach builds from goals backwards — we met together to outline short and long-term goals and then used those goals to create a plan across a variety of decisions, from home ownership to car insurance to investment and much more. Richard and Emily truly do a great job of drawing me into the loop, ensuring that the financial plan we develop reflects my goals and wishes. Before settling with Archer Investments, I talked with a number of other advisors and none of them had the combination of professionalism, attention to detail, and comprehensive services offered by Archer.

Ben

Received via WealthTender: July 1, 2024

I’m not finance-oriented by any measure, but luck came my way for once and I found myself having enough assets to need some help. Only I didn’t know what kind of help I needed and it’s easy to get overwhelmed quickly and I was on like year number whatever of being overwhelmed and I just kicked that can down the road every year. After a short search, I found Archer’s team and quickly just pushed other options off the table and signed on. They’ve actually been able to simplify things in a way that makes me feel like I can manage my life and not worry about it all for the first time in years. I basically had all eggs, but no basket. Now I have a comprehensive plan from some incredible staff and I actually love the process instead of dreading the matter. Simply put, Archer has changed how I view my own finances and what used to be a cause of stress for me is now a giant sigh of relief. I said in the title it was the best decision ever and I mean it: this has 100% seriously no-fingers-crossed changed my life. If you’re like me and you’ve been debating if you even need this kind of help, then yes… yes, you do!

Scott Eaton

Received via WealthTender: July 10, 2024