Pre-IPO SpaceX planning starts with knowing exactly what you own, how concentrated you are, and what liquidity may or may not be available.

The biggest risks usually involve taxes, timing, and having too much of your net worth tied to one company before an IPO or tender window opens.

A strong plan should be built in stages, coordinated with the right advisors, and documented before emotions or tight deadlines drive decisions.

If SpaceX equity makes up a large portion of your net worth, pre‑IPO planning isn’t about optimizing returns, it’s about managing risk, taxes, and optionality before liquidity arrives.

This checklist reflects the most common issues we see among SpaceX employees as equity values grow and decisions become harder to reverse.

You don’t need to act on everything at once, but you do want to understand the full picture before a narrow liquidity window opens.

1. Inventory Your SpaceX Equity (Know What You Actually Own)

Before any strategy discussion, get clarity on the basics:

Number of shares owned (vested vs unvested)

Option types (ISOs, NSOs)

Exercise dates and prices

Cost basis and holding periods

Transfer restrictions or consent requirements

Exposure through prior tender offers or side vehicles

Many planning mistakes happen simply because this information isn’t centralized.

Talk to your financial advisor to understand how this applies to your personal situation.

4. Review Tax Exposure Early (Before Decisions Are Forced)

Key questions to evaluate in advance:

What is my estimated capital gains exposure at IPO pricing?

How does AMT factor into my option history?

Would staged diversification materially reduce tax impact?

How does my state residency affect outcomes?

Tax strategies are far more effective before liquidity, not after.

5. Evaluate Diversification Tools (and Their Trade‑Offs)

Common strategies to consider pre‑IPO:

Holding a concentrated position for upside

Options overlays to manage downside risk

Section 351 exchanges for diversification with tax deferral

Exchange funds with long lockups

Charitable planning for highly appreciated shares

Each involves trade‑offs around control, liquidity, fees, and future taxes. There is no default “right” answer.

6. Stress‑Test Liquidity Needs

Ask:

How much true liquidity do I need in the next 1–3 years?

Do I have sufficient cash outside SpaceX equity?

Are upcoming expenses (home, taxes, family, lifestyle) funded?

Illiquid wealth creates stress, even when headline net worth is high.

7. Revisit Risk Tolerance Honestly

Risk tolerance often changes as numbers get bigger.

How would I feel if SpaceX represented 80%+ of my net worth at IPO?

Would volatility affect decision‑making or sleep?

Do I want certainty, flexibility, or maximum upside?

Planning should match behavior, not just math.

8. Coordinate Advisors Early

Pre‑IPO planning works well when advisors collaborate before decisions are locked in.

Financial planner with equity‑comp expertise

Tax advisor familiar with stock‑based compensation

Legal counsel for transfer or fund structures

Misalignment between advisors often creates unnecessary cost and complexity.

9. Build a Staged Plan, Not a Single Bet

For most SpaceX employees, diversification works efficiently when approached in phases:

Pre‑IPO risk management

Initial liquidity event planning

Tax‑aware diversification over time

Post‑IPO portfolio construction

Optionality is often more valuable than precision.

10. Document the Plan (So Emotions Don’t Drive Decisions)

Finally:

Write down your assumptions

Define thresholds for action

Set expectations before emotions are involved

Revisit and update annually

When liquidity arrives, decisions may happen fast. The plan should already exist.

Final Thought

Being pre‑IPO at SpaceX is exciting—but it creates complexity many tech professionals rarely face.

Thoughtful planning ahead of liquidity can help you make more informed decisions, maintain flexibility, and reduce the risk of rushed choices. Regardless of when or how SpaceX ultimately goes public.

Our team of CERTIFIED FINANCIAL PLANNER® professionals (serving clients nationwide, virtually) works with SpaceX employees to help them understand their equity, explore their options, and build personalized financial plans around what matters most to them.

If a large portion of your net worth is tied to SpaceX stock, a thoughtful plan can help you think more clearly about taxes, liquidity, concentration risk, and what this wealth is meant to do for your life.

Book a call to build a thoughtful plan for your SpaceX equity, so you can worry less about money and focus more on the life you are building.

This article is for general educational purposes only and is not individualized tax, legal, or investment advice. Tax rules are complex and can change, and outcomes depend on your specific situation. You should consult your CPA and/or attorney regarding your circumstances. Archer Investment Management is an SEC-registered investment adviser; registration does not imply a certain level of skill or training. Investing involves risk, including the possible loss of principal.

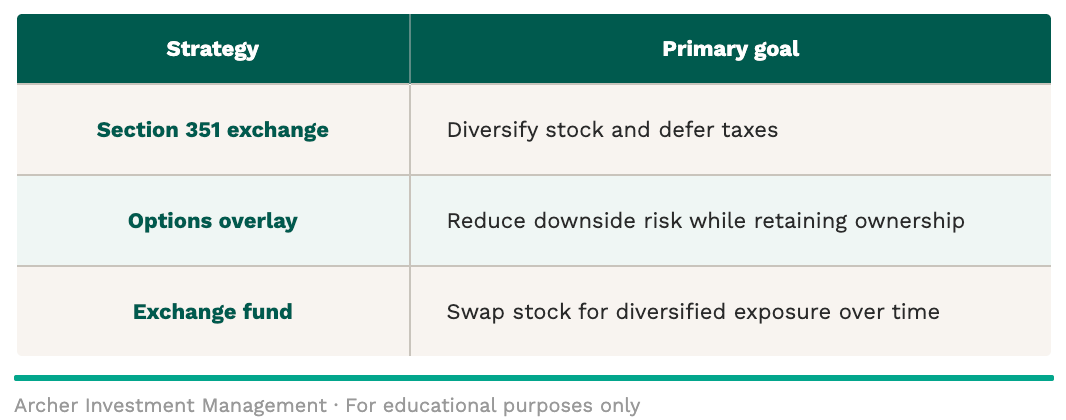

Pre-IPO SpaceX employees have several ways to reduce concentration risk, but each strategy solves different trade-offs.

Section 351 exchanges, options overlays, and exchange funds all involve trade-offs around taxes, control, liquidity, complexity, and upside potential.

The right approach usually depends less on finding the “best” strategy and more on choosing the trade-offs that fit your goals, timeline, and risk tolerance.

Once SpaceX equity becomes a meaningful part of your net worth, diversification stops being a theoretical concept and starts feeling urgent.

All three aim to reduce single‑stock risk—but they work in very different ways, with very different trade‑offs. Understanding those differences is critical before committing to any one approach. Let’s break them down.

Big Picture: Three Paths to Managing Concentration Risk

At a high level, these strategies answer different questions:None is universally “better.” Each fits different priorities around taxes, control, liquidity, and complexity, especially important considerations before an IPO.

None is universally “better.” Each fits different priorities around taxes, control, liquidity, and complexity, especially important considerations before an IPO.

Talk to your financial advisor to understand how this applies to your personal situation.

Section 351 Exchanges: Structural Diversification with Tax Deferral

A Section 351 exchange allows you to contribute SpaceX shares into a newly created entity in exchange for ownership in a diversified investment vehicle—without triggering immediate capital gains taxes.

A Section 351 plan is often the most aggressive diversification tool, but also the least flexible.

Options Overlays: Risk Management Without Selling Stock

Options overlay strategies (such as collars or covered calls) use derivatives to define downside risk and/or generate income, while allowing you to continue owning your SpaceX shares.

For pre‑IPO employees, these are sometimes used when liquidity events are expected, but timing remains uncertain.

Best for pre‑IPO SpaceX employees who:

Want to retain ownership and control

Are comfortable with complexity

Expect future liquidity (IPO or tender)

Prefer incremental risk reduction

Key advantages

No sale of shares

Retains upside (to a point)

Can reduce volatility or generate income

Trade‑offs

No true diversification

Requires ongoing management

Costs can erode returns

May cap upside during major positive events

Options overlays manage risk, not concentration. Your net worth is still tied to SpaceX.

Exchange funds pool stock from multiple investors and allow participants to exchange their concentrated shares for interests in a broadly diversified fund.

Unlike Section 351 exchanges, many exchange funds are long‑standing vehicles with predefined structures.

Best for pre‑IPO SpaceX employees who:

Want diversification without selling

Can tolerate long lockups

Are comfortable with limited transparency

Don’t need near‑term liquidity

Key advantages

Diversification without immediate taxes

Exposure to a portfolio of other stocks

Familiar structure for many high‑net‑worth investors

Trade‑offs

Very limited liquidity (often 7+ years)

Less control over holdings

Fees and structural constraints

Concentration can still re‑emerge at exit

Exchange funds can feel intuitive, but they are not liquid solutions, and exits often arrive later and differently than investors expect.

How Pre‑IPO SpaceX Employees Typically Combine These Strategies

In practice, most SpaceX employees don’t choose just one. Instead, diversification tends to happen in stages, as liquidity options evolve:

Early career: tolerate concentration, build cash reserves

Pre‑IPO maturation: evaluate options overlays or partial transfers

Liquidity events: layer in direct sales and tax planning

Post‑IPO: reassess full portfolio diversification

Section 351 plans may play a role, but often alongside more flexible tools that preserve future optionality.

There’s No “Best” Strategy; Only the Right Trade‑Off For You

The most common mistake we see is evaluating these strategies in isolation. The real question isn’t:“Which strategy is best?” It’s: “Which set of trade‑offs am I most comfortable living with?”

For pre‑IPO SpaceX employees, trade‑offs around liquidity, control, taxes, and risk tolerance matter more than theoretical returns.

Our team of CERTIFIED FINANCIAL PLANNER® professionals (serving clients nationwide, virtually) works with SpaceX employees to help them understand their equity, explore their options, and build personalized financial plans around what matters most to them.

If a large portion of your net worth is tied to SpaceX stock, a thoughtful plan can help you think more clearly about taxes, liquidity, concentration risk, and what this wealth is meant to do for your life.

Book a call to build a thoughtful plan for your SpaceX equity, so you can worry less about money and focus more on the life you are building.

This article is for general educational purposes only and is not individualized tax, legal, or investment advice. Tax rules are complex and can change, and outcomes depend on your specific situation. You should consult your CPA and/or attorney regarding your circumstances. Archer Investment Management is an SEC-registered investment adviser; registration does not imply a certain level of skill or training. Investing involves risk, including the possible loss of principal.

A SpaceX IPO can make your equity feel more valuable overnight, but lock-ups and trading restrictions may still limit what you can actually do with it.

Concentrated stock creates more than just investment risk. It can also make tax planning, diversification, and timing much harder during a narrow decision window.

For some high-income employees, advanced planning strategies may help create more flexibility and make post-IPO decisions more manageable.

For many SpaceX employees, especially high-earning tech professionals, an IPO won’t necessarily create immediate freedom. But it will create a new layer of complexity.

Your equity may suddenly have a public market price, but lock-up restrictions and trading windows can still often delay when you’re actually able to sell.

That can leave many employees in a frustrating position during IPO year: a large portion of their net worth is visible and market-priced, but still not liquid.

That is why SpaceX IPO lock-up planning matters.

The goal isn’t just to react when the lock-up ends. It’s to make thoughtful decisions before taxes, concentration risk, and market volatility all start showing up at once.

This article focuses on one advanced planning tool some high-income investors and tech executives may use in that window: a tax-managed long/short strategy.

Talk to your financial advisor to understand how this applies to your personal situation.

The Problem: Concentrated Stock and IPO Timing

For many employees, SpaceX IPO planning unfolds in three phases:

1. Before the IPO

Your equity has value, but liquidity is still uncertain.

Your stock may now have a public market price, but selling can still be restricted for a period that is often around 180 days.

3. After the Lock-Up Ends

Liquidity may finally arrive, but taxes, concentration risk, and emotional decision-making often become more immediate.

One of the biggest planning mistakes is waiting until the lock-up ends to act.

By then, the stock is public, the value is visible, and the pressure to make the “right” decision can feel much higher. That is often when volatility, tax consequences, and concentrated-stock risk all start to collide.

What Is a Tax-Managed Long/Short Strategy?

A tax-managed long/short strategy is an advanced investment approach used within a taxable portfolio.

It combines long positions and short positions in a way that aims to keep overall market exposure similar to a more traditional equity allocation while increasing the opportunity to harvest capital losses over time.

In plain English, the benefit is not that it makes taxes disappear. It’s that it could create more flexibility later if you need capital losses to help offset gains from selling concentrated stock.

For example, for some SpaceX employees, that could be useful when a large portion of their net worth is tied up in low-basis company stock, and selling too much at once could create a meaningful tax bill.

Why This Can Matter for SpaceX Employees

If you hold a large amount of low-basis SpaceX stock, diversification may feel harder than it sounds. On paper, selling shares reduces concentration risk, but in practice, selling can also trigger substantial capital gains and a large tax cost.

That tax friction is just one reason some employees hold concentrated stock longer than they really want to.

A tax-managed long/short strategy is sometimes used to help create more flexibility by:

Building a reserve of potential capital losses over time

Creating losses that may help offset future capital gains

Supporting a more gradual, tax-aware path to diversification

Reducing the pressure to sell too much, too quickly, in a narrow post-lock-up window

Again, this approach does not eliminate taxes or remove market risk, but in the right situation it could help make diversification more manageable.

How Long/Short Can Fit Into the SpaceX IPO Timeline

In some cases, a tax-managed long/short portfolio may be funded with cash or other taxable assets, so it’s already in place before SpaceX shares become sellable.

During the IPO and Lock-Up Period

This is often the most uncomfortable phase. Your equity may have a visible market value, but your ability to act on it is still limited.

During that time, a tax-managed long/short portfolio can continue operating independently and may continue harvesting losses if market conditions allow, even while SpaceX shares remain restricted.

After the Lock-Up Ends

Once shares become sellable, previously harvested losses may help offset gains from staged sales of SpaceX stock. Over time, leverage may be reduced, and the portfolio may transition toward a more traditional long-only structure as concentration risk declines.

That is why exit planning matters.

A tax-managed long/short strategy shouldnotbe treated as a permanent add-on without a clearly defined purpose. It should be part of a broader plan for reducing concentration risk over time.

A thoughtful SpaceX IPO lock-up planning process could help you:

Avoid feeling forced to sell too much at once

Create more flexibility around when and how to diversify

Manage taxes more deliberately over time

Reduce stress that often comes from having too much wealth tied to one stock

Make decisions with more clarity during a period that can feel emotionally charged

That is the bigger point. The goal is not to find a perfect strategy but to reduce the odds of rushed decisions at exactly the moment when the stakes feel highest.

Important Tradeoffs to Understand

Tax-managed long/short strategies are advanced and may not suit every investor.

They can involve:

Leverage and margin

Higher complexity than traditional long-only investing

Additional costs

Active risk management

The need for a clearly defined exit or deleveraging plan

This strategy is generally best suited for high-income investors with large taxable portfolios and significant concentrated stock exposure. They also require careful coordination with the rest of the financial plan, including tax planning, liquidity needs, and the timeline for reducing concentration risk.

The Bigger Planning Goal

For many SpaceX employees, the real goal during this time is to reduce concentration risk, manage taxes thoughtfully, and create more flexibility during the period when the stock is public but life still feels uncertain.

A tax-managed long/short strategy is just one tool some investors use toward that end. In the right situation, it may help make diversification more gradual and more tax-aware. But like any advanced strategy, it works best when it is part of a larger financial plan rather than a standalone tactic.

Ready to Build a SpaceX IPO Tax-Managed Long/Short Strategy?

Our team of CERTIFIED FINANCIAL PLANNER® professionals (serving clients nationwide, virtually) works with SpaceX employees to help them understand their equity, explore their options, and build personalized financial plans around what matters most to them.

Book a call to build a thoughtful plan for your SpaceX equity, so you can worry less about money and focus more on the life you are building.

If a large portion of your net worth is tied to SpaceX stock, a thoughtful plan can help you think more clearly about taxes, liquidity, concentration risk, and what this wealth is meant to do for your life.

This article is for general educational purposes only and is not individualized tax, legal, or investment advice. Tax rules are complex and can change, and outcomes depend on your specific situation. You should consult your CPA and/or attorney regarding your circumstances. Archer Investment Management is an SEC-registered investment adviser; registration does not imply a certain level of skill or training. Investing involves risk, including the possible loss of principal.

If a large chunk of your net worth is tied to SpaceX stock, an option overlay strategy may let you manage your risk without triggering a big tax bill.

Your lock-up period is actually planning time. Use it.

The goal isn’t a perfect exit. It’s to have a clear plan in place so you’re not making major financial decisions under pressure.

With a potential SpaceX IPO having been widely discussed as early as June, many SpaceX employees are asking the same questions about SpaceX IPO option overlay strategies:

What happens if the stock drops after the IPO?

How do I reduce risk without blowing up my tax situation?

Is there a way to potentially diversify without selling everything right away?

If you’re a SpaceX employee and a large portion of your net worth is tied to SpaceX stock (through options, RSUs, or early-stage shares), you’re in a classic “concentrated‑wealth” scenario.

And while an IPO can be an exciting milestone, it may also introduce volatility, lock-ups, and significant tax exposure.

This article is for general educational purposes only and is not individualized tax, legal, or investment advice. Please consult your CPA and/or attorney regarding your specific circumstances.

The Unique Risks SpaceX Employees May Face Before an IPO

Pre-IPO equity can have several defining characteristics worth understanding before a liquidity event:

Extreme concentration: Your income and net worth may both be tied to the same company.

Low or near-zero cost basis: In plain terms, you may have shares that are worth a lot more than you paid for them, which means selling could trigger a large tax bill.

Timing constraints: lock-ups, blackout periods, and market volatility may limit your flexibility to act when you want to.

This is where option overlay strategies become especially relevant, and these are exactly the kinds of challenges we help tech professionals think through.

What Are SpaceX IPO Option Overlay Strategies (and How Are They Different From Selling?)

Think of an option overlay as a way to put a financial structure around stock you already own without having to sell it.

It uses exchange-listed options (most commonly puts and calls) to potentially manage risk, create cash flow, and improve tax outcomes.

Some general characteristics of these strategies include:

You may be able to keep your shares

They do not automatically trigger capital gains, though tax treatment depends on your specific situation

Strategies can be tailored around an IPO window, lock-up period, and post-IPO plans

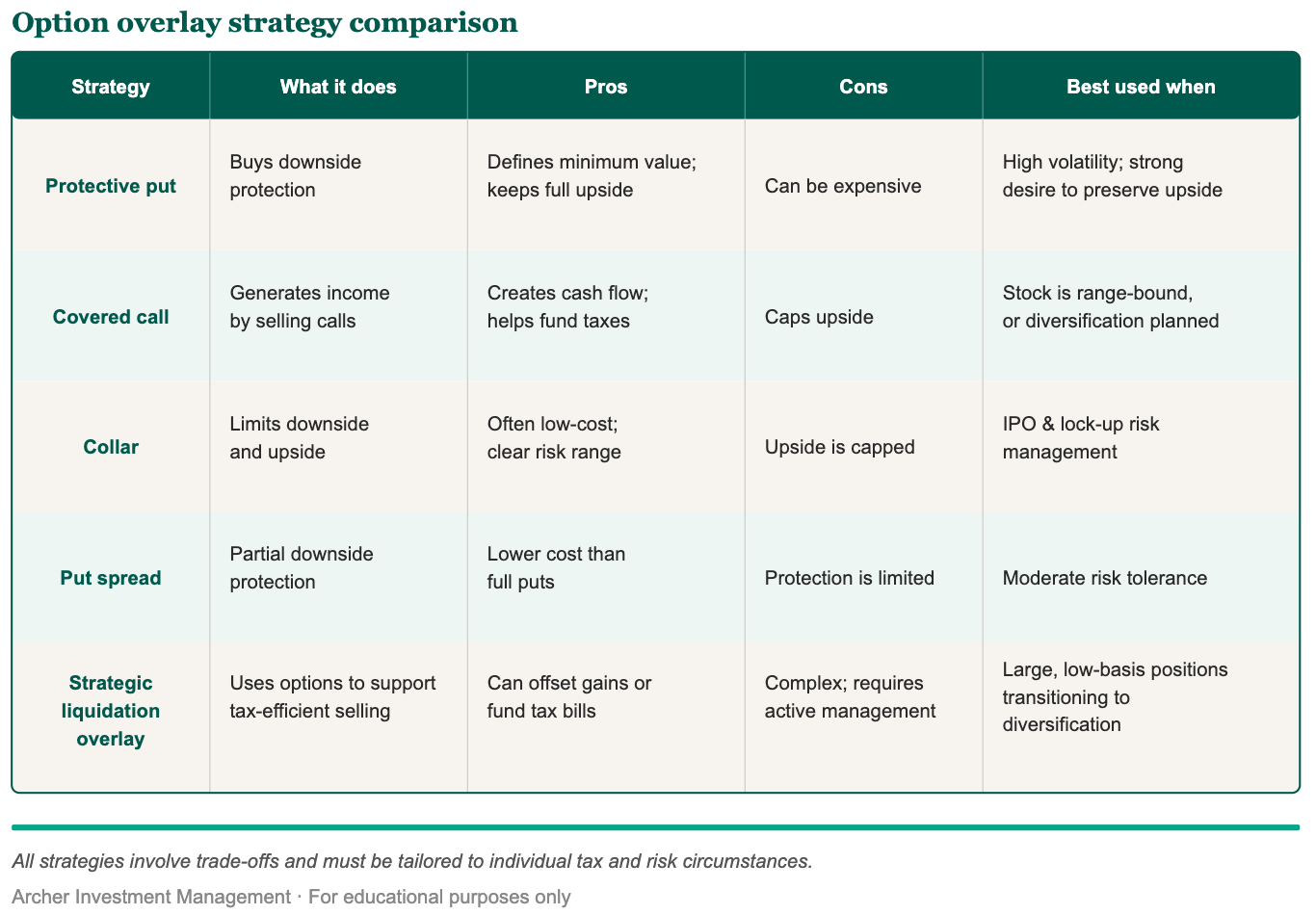

Common Option Overlay Strategies for SpaceX Employees

Below is a high‑level comparison of the most commonly used option overlay strategies around IPOs:

This is not a recommendation of any specific strategy. Talk to your financial advisor to understand how this applies to your personal situation.

What Option Overlay Strategies Don’t Do

It’s important to set clear expectations:

Option overlays do not eliminate risk entirely

Upside potential may be limited in exchange for downside protection

They require professional execution and ongoing monitoring

Tax treatment is not guaranteed and depends on individual circumstances

Past performance of any strategy is not indicative of future results

These strategies are most appropriate for investors who value planning, risk management, and tax awareness over short‑term speculation.

FAQ

What happens if SpaceX stock drops after the IPO?

Markets around IPOs can be unpredictable, and if a large portion of your net worth is tied to SpaceX stock, a drop in the share price can have an outsized impact on your overall financial picture.

Certain option overlay strategies, such as protective puts or collars, may help define your risk during periods of uncertainty.

How do I reduce risk without blowing up my tax situation?

For employees with low or near-zero cost basis, selling shares outright may trigger a significant tax bill.

An option overlay strategy may allow you to put a financial structure around stock you already own without having to sell it immediately.

Depending on the strategy and individual circumstances, option overlays can also support tax-aware diversification over time.

Is there a way to potentially diversify without selling everything right away?

Rather than a single high-stress exit, option overlay strategies can support a multi-phase transition over time.

In practical terms, this can allow SpaceX employees to begin diversifying earlier and more efficiently than relying on outright sales alone, while selling shares more strategically over time and reinvesting into a diversified, lower-risk portfolio.

Ready to Build a SpaceX IPO Option Overlay Strategy?

A June SpaceX IPO represents a once‑in‑a‑career financial milestone for many employees at this company.

The biggest risk often isn’t even the IPO itself, it’s what happens after if no strategy is in place.

Having a thoughtful strategy in place before a liquidity event can help you make more informed decisions about risk, taxes, and diversification.

Our team of CERTIFIED FINANCIAL PLANNERs® work with tech professionals, including SpaceX employees, to help them understand their equity, explore their options, and build personalized financial plans around what matters most to them.

If you’re a SpaceX employee wondering whether an option overlay strategy might make sense for your situation, book a call with our team.We’d love to connect.

This article is for general educational purposes only and is not individualized tax, legal, or investment advice. Tax rules are complex and can change, and outcomes depend on your specific situation. You should consult your CPA and/or attorney regarding your circumstances. Archer Investment Management is an SEC-registered investment adviser; registration does not imply a certain level of skill or training. Investing involves risk, including the possible loss of principal.

Your SpaceX equity is not a single asset: RSUs, ISOs, and NSOs each carry different tax implications, and understanding the difference can meaningfully change your outcome.

Your state of residency at the time of the IPO can shift your tax bill by hundreds of thousands of dollars. It’s worth planning for before the window closes.

A strong financial plan goes beyond taxes. It’s about making sure your entire financial picture is positioned to make the most of this opportunity.

If you work at SpaceX, a large chunk of your net worth might exist in SpaceX equity, which can make that money feel more theoretical than tangible. But if an IPO happens, that “future money” can suddenly create very real decisions around taxes, liquidity, concentration risk, and timing.

Even after an IPO, employees and insiders are often subject to lockup agreements that could restrict selling for about 180 days. Your net worth could become “market priced” before it becomes “liquid.”

For many high-earning tech professionals, this is where success starts to feel stressful. The value is real, but the path forward is not always clear.

Your SpaceX Equity Is Not One Asset

One of the big mistakes employees can make is treating SpaceX equity like it’s “one thing” aka a single asset.

In reality, it is often a mix of private shares, stock options, and RSUs…and each one has different tax landmines:

RSUs are generally taxed like wages when they vest. Think of it like a cash bonus paid in stock. You may have capital gains or losses after vesting if you hold and sell later.

ISOs may trigger AMT when exercised, even if you don’t sell (a “phantom tax” problem).

NSOs typically generate ordinary income at exercise.

High earners often model long‑term capital gains at the top federal rate plus the 3.8% net investment income tax (NIIT) once income exceeds the NIIT thresholds, including $250,000 for married filing jointly (MFJ).

Case Study: Maria, 50 — $6M in Pre-IPO Equity and No Plan Yet

Meet Maria. She’s 50, married filing jointly, with two young children ages 6 and 8. She holds $6 million in pre‑IPO SpaceX equity and hasn’t done much planning. Because it doesn’t feel real yet.

This is more common than most people realize. When your wealth is tied up in shares you can’t sell, it’s easy to delay planning. But IPO year is often when that uncertainty turns into pressure.

Suddenly, RSU withholding may fall short. ISO exercises may create AMT exposure. Lockup rules may delay access to the liquidity you would use to pay taxes or reduce risk.

Maria’s question isn’t just “What will I owe?” It’s “How do I make smart decisions now without creating regret later?”

What the Tax Picture Could Look Like

Let’s look at a simple illustration of what taxes could look like once liquidity exists. The point is not to create fear, it’s to make the tradeoffs easier to see before the stakes get higher.

Federally, high earners commonly model 20% long‑term capital gains + 3.8% NIIT (NIIT applies once MAGI exceeds thresholds like $250,000 MFJ).

And because lockups can restrict selling for ~180 days after IPO, one of the best planning moves is simply to build a tax reserve and liquidity runway now. So you’re not forced into rushed decisions the moment the window opens.

The examples given are for illustrative purposes only. Speak with a financial planner to understand how the tax triggers, gains, and impacts apply to your situation.

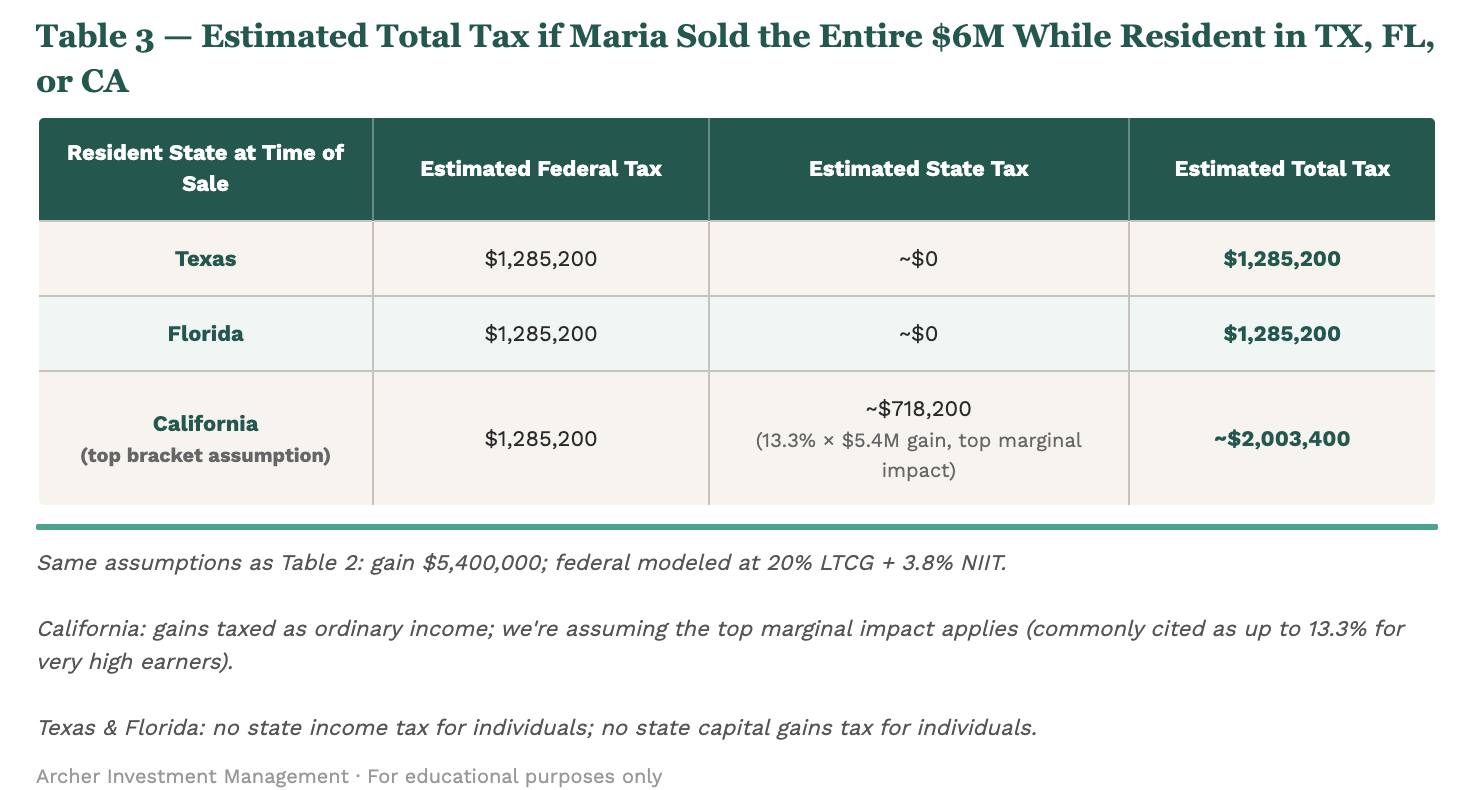

The State-Tax Swing: Why Residency Matters in SpaceX IPO Planning

Where you live can make a big difference in how much you actually keep after taxes.

For example, California taxes capital gains at ordinary income rates for state tax purposes. Yet, Florida and Texas have no state income tax for individuals.

So if a major liquidity event is coming, your state of residency at the time of sale can meaningfully affect how much of your IPO liquidity you keep.

The illustration below shows just how wide that gap can be.

A practical note here: residency planning has to be real. It is not about a last-minute change on paper. If a move is already under consideration, it usually needs to be handled correctly and early enough to matter.

“Do I have to sell everything at once?”

Usually, no.

A thoughtful SpaceX IPO planning strategy aims to:

Avoid tax surprises

Reduce the risk of having “too much in one stock”

Respect lockups and trading windows

A common risk-management tool for concentrated stock is a collar strategy (own the stock, buy a protective put, sell a covered call) to define a floor and ceiling for a period of time. This is helpful when you want downside protection without immediately selling everything.

If you’re subject to blackout windows or insider restrictions, a Rule 10b5‑1 trading plan may help. It creates a disciplined selling approach once trading is permitted, with rules like cooling‑off periods and good-faith requirements.

The goal isn’t to time everything perfectly. It’s to make steady, informed decisions you can feel good about.

IPO Wealth Is a Life-Planning Moment

IPO wealth is not just an investment issue. It’s a moment that touches your entire financial life.

For Maria, that means more than building a tax-smart equity strategy. It also means making sure the rest of her financial life is ready for what this wealth could make possible.

We would review estate documents, including guardianship language for her children, wills, trusts, and powers of attorney. We’d build a college funding plan that supports her kids without putting her retirement at risk. We’d also review umbrella liability coverage, since a higher net worth can increase the financial impact of everyday risks.

All of that connects back to the equity plan itself. RSUs vest and create tax events while ISOs can trigger AMT.

A strong financial plan connects those moving pieces, so Maria can make decisions with more clarity, avoid unnecessary surprises, and use her SpaceX equity in a way that supports her family and her long-term goals.

Ready to Turn Your SpaceX Equity Into a Clear Plan?

If you’re a SpaceX employee with a large portion of your net worth tied to SpaceX stock, thoughtful planning can help you do more than prepare for taxes.

It can help you make smarter decisions about liquidity, risk, and what this wealth is meant to do for your life.

We help clients turn complex equity compensation into a clear strategy, so they can feel more confident about their money and more free to focus on what comes next.

Schedule a call with our team, which specializes in financial planning for tech executives to turn your SpaceX equity into a clear plan, so you can worry less about money and focus more on the life you’re building.

This article is for general educational purposes only and is not individualized tax, legal, or investment advice. Tax rules are complex and can change, and outcomes depend on your specific situation. You should consult your CPA and/or attorney regarding your circumstances. Archer Investment Management is an SEC-registered investment adviser; registration does not imply a certain level of skill or training. Investing involves risk, including the possible loss of principal.

At Archer Investment Management, we help tech professionals and pre-retirees gain clarity and confidence about their financial futures — so they can worry less about money and focus more on enjoying the life they’ve worked hard to build.

Many of our clients are high earners navigating tech equity compensation, IPO windfalls, and high-stress roles, or individuals preparing for retirement who want a smooth and confident transition.

What makes us unique as financial advisors is our belief that money isn’t just math — it’s deeply connected to your decisions, your dreams, and sometimes even your worries.

That’s why we design financial plans that don’t just prepare you for the future, but also make your life feel better today.

By weaving together financial planning, tax strategies, and investment management with proactive guidance, we help clients replace stress and second-guessing with clarity, confidence, and more room for the things that matter most.

The result is a clear plan that reduces stress and creates flexibility in your financial life.

Whether you’re aiming to retire early, shift into more fulfilling work, or maximize the wealth you’ve worked so hard to build.

Here’s what clients say about working with Archer:

“I was quite literally afraid of getting help and of all that it involved. It’s been wonderful. No kidding: best decision ever!

I’m not finance-oriented by any measure, but luck came my way for once and I found myself having enough assets to need some help. Only I didn’t know what kind of help I needed and it’s easy to get overwhelmed quickly and I was on like year number whatever of being overwhelmed and I just kicked that can down the road every year.

After a short search, I found Archer’s team and quickly just pushed other options off the table and signed on. They’ve actually been able to simplify things in a way that makes me feel like I can manage my life and not worry about it all for the first time in years. I basically had all eggs, but no basket. Now I have a comprehensive plan from some incredible staff and I actually love the process instead of dreading the matter.

Simply put, Archer has changed how I view my own finances and what used to be a cause of stress for me is now a giant sigh of relief. I said in the title it was the best decision ever and I mean it: this has 100% seriously no-fingers-crossed changed my life. If you’re like me and you’ve been debating if you even need this kind of help, then yes… yes, you do!”

Disclosure: These testimonials were provided by current Archer Investment Management clients and may not be representative of the experiences of other clients. The clients were not compensated, nor are there material conflicts of interest that would affect the given testimonials. View more reviews on WealthTender or Google.

That said, we know we aren’t the right fit for everyone. That’s why we’ve compiled this list of other respected financial advisors in Austin for 2026 to help you find the right match for your unique situation.

Disclaimer: This list is not exhaustive. It reflects our opinion only and should not be considered a testimonial or endorsement of any advisor included.

Other Top Financial Advisors in Austin in 2026

1. LeafHouse Financial

Specialty:

High-net-worth families

Institutional retirement plans

Why They Stand Out: LeafHouse is one of Austin’s largest independent RIAs, managing over $2 billion in assets. They’re known for their retirement plan investment management expertise, fiduciary advice, and proprietary technology platform that streamlines complex portfolio oversight.

2. Reap Financial

Specialty:

Entrepreneurs

Families focused on legacy planning

Why They Stand Out: Reap operates as a “virtual family office,” guiding clients through tax strategy, estate planning, retirement income, and investments. They’re particularly strong for entrepreneurs and affluent families who want to preserve and grow wealth across generations.

“Chris and his team enabled me to retire and continue to enjoy a very comfortable lifestyle.Their level of professionalism, fiscal knowledge and integrity is very hard to find in these competitive times. Reap Financial guided us through the many investment loopholes, ensuring we placed our savings in the right buckets.

For anyone looking for financial peace of mind in their later years, I would not hesitate to recommend Chris and his team at Reap Financial.”

Holistic wealth planning with ongoing client access

Why They Stand Out: Austin Wealth emphasizes collaboration and education. Clients gain access to a secure wealth management system to track progress, paired with regular check-ins and proactive communication.

4. DESMO Wealth Advisors

Specialty:

Fee-only financial planning informed by behavioral economics

Why They Stand Out: Led by Dr. Massi de Santis, Ph.D. and CFP®, DESMO integrates behavioral economics into comprehensive, fee-only planning. Their approach helps clients identify and overcome biases that can derail financial progress.

5. Elgon Financial Advisors

Specialty:

Immigrants

Professionals with equity compensation

Why They Stand Out: Founded by Jane Mepham, CFP®, Elgon focuses on immigrant families and professionals navigating equity compensation. Jane’s IT background and personal immigrant experience give her unique insight into the challenges these clients face.

“Jane is not only a great financial advisor but also knowledgeable, kind, and hard working.

She’s ready to do the research to help advise on tricky financial decisions or provide the depth of knowledge she already has on cross-border financial advice.

Austin is home to a wide range of excellent financial advisors, each with unique specialties and strengths. If you’re looking for guidance, you have strong options across the city.

We help clients reduce stress, create flexibility, and build an intentional financial plan that supports the life they want to live today and tomorrow.

RSUs and restricted stock are valuable, of course, but they do come with tax and planning decisions. Start by knowing your goals and your vesting schedule, then go from there.

2 words: game plan. It’s absolutely crucial to understand your vesting schedule and create a strategy for when to sell. Use strategies like tax deferral and diversification to keep more of your earnings (and don’t let surprise taxes or market dips catch you off guard!).

Don’t let too much of your portfolio be tied up in company stock (this is actually a risk). Instead, have a plan for when to sell and how to reinvest. Diversifying can help you stay in control.

Incorporating restricted stock and RSUs (restricted stock units) into your financial plan can get complicated. You will need to make plenty of decisions, such as how long you will hold your shares if you should sell them and put them into an alternative investment, or if you will use the money to meet one of your financial goals.

If your head is spinning, take heart. Here are 10 simple tips to help you maximize your restricted stock and RSUs.

Before We Start, How Do RSUs Work Again (And How Does This Differ From Restricted Stock)?

Restricted stock units (RSUs) are a form of equity compensation that companies grant to employees, in which the employees receive company shares upon completion of a specified vesting schedule. Think of them as a bonus – paid in stock shares instead of cash.

They differ from stock options in that employees do not have to purchase shares at a particular stock price; rather, they are given shares outright once they vest.

By contrast, “restricted stock” is actual stock granted on the award date, but it generally cannot be sold or transferred until it vests. Because you technically own restricted stock at grant (although with restrictions), it may be eligible for dividends and potentially an 83(b) election.

RSUs and restricted stock tie employee interests to the company’s future performance.

However, if you’re not sure how to fit either of these into your overall financial plan, the following rules should help guide you in determining an ideal approach.

Rule #1: Set Your Goals For Your RSU or Restricted Stock Strategy

In order to make quality decisions, you need to determine what you hope your stock will do for you.

When you eventually sell the shares, where do you want that money to go? How do your shares and their potential sale fit in relation to your other income, 401(k), and other savings?

When setting your objectives, keep both your timelines and your financial goals in mind. Whether you have restricted stock or RSUs, these awards can help fund key financial priorities, such as:

Paying for education

Providing a down payment on a home

Growing retirement savings

Diversifying existing investments

By outlining these aims at the outset, you’ll be able to make more informed choices about whether to hold, sell, or reinvest your shares.

You should also consider how RSUs fit into your broader compensation, especially if they represent a large portion of your earning potential. Be sure to keep them on your radar alongside salary, bonuses, and any other benefits you receive.

Rule #2: Know Your Vesting Schedule

It is important to know the dates your grants will vest since you will need to pay taxes on the resulting income.

If you want to avoid a hefty tax bill, it requires planning ahead. Your vesting schedule will depend on your company and the conditions they place on the stock, but it is usually time-based, requiring you to work at the company for a certain period before vesting can occur.

One helpful approach is to create a timeline or calendar event marking each vest date. By planning around these dates, you’ll have a clearer picture of how your income may spike during certain periods, potentially moving you into a higher tax bracket.

You might also want to see if your company offers any flexibility in your vesting; for instance, some companies allow for acceleration of vesting in certain circumstances, such as mergers, acquisitions, upon disability, or retirement eligibility.

Either way, thinking ahead helps with tax planning and allows you to anticipate your tax liability (the amount you’ll need to pay the government when tax time comes) long before you owe it.

📝 Note: Tax liability is a fancy word for the amount of money you owe in taxes to the government.

Rule #3: Understand the Consequences if You Were to Quit

If you leave your company before your restricted stock vests, you will usually forfeit the unvested grants.

There can be exceptions to this, so be sure to gather all the details from your company before you make the decision to leave.

If you have a significant amount of shares that haven’t vested, it might be worth it to stay with your company long enough to benefit from this reward for your service.

Evaluate the current and future value of your RSUs or restricted stock and think about whether staying at the company until a certain vest date could be financially advantageous. If you are planning a career change, weigh the opportunity cost of leaving unvested RSUs behind against the benefits of a new role.

Sometimes, negotiations with a new employer could include a ‘make-whole’ RSU or stock grant to compensate you for the value you are giving up.

Rule #4: Consider Taxes

Your taxable income will be the market value of the shares at vesting and is subject to federal income tax, Social Security, and Medicare, plus any state and local income tax.

📝 Note: Taxable income is the part of your income that the government uses to figure out how much tax you owe.

Your company may offer you a few ways to pay taxes at vesting, such as withholding shares for taxes, a sell-to-cover transaction for taxes of a portion of the shares, a salary deduction, or simply a check payment. A 22% standard supplement tax withholding, as a sale from shares vested is fairly common. The standard withholding rate often becomes 37% if your total income exceeds $1,000,000.

When you eventually sell the shares, you will pay capital gains tax on any appreciation the stock has from the vest date until the sale date.

To further minimize your overall tax liability, consider increasing contributions to tax-deferred accounts—such as 401(k)s, Health Savings Accounts (HSAs), or other qualified plans—during your vesting years. By carefully coordinating these strategies, you can maintain more control over your income and keep your total tax liability in check.

Rule #5: Look Into an 83(b) Election

With restricted stock (not RSUs), you have the option to make a Section 83(b) election with the IRS within 30 days of the grant date.

An 83(b) election allows you to pay taxes on the value of the stock at the grant date rather than the vesting date.

If you believe the stock price will be higher on the vesting date and you are confident you will meet vesting requirements, this can be a beneficial move for you.

Also, moving the time of taxation to the grant date starts the capital gains holding period earlier, which can make a difference at the eventual sale of the shares.

However, keep in mind that making an 83(b) election does involve certain risks: if the stock doesn’t appreciate or—worse—loses value, you might have paid more taxes upfront than necessary. Additionally, if you leave the company or fail to meet vesting requirements, you generally cannot get a refund on taxes already paid because the election is irrevocable once filed. It’s important to consult with a tax advisor or financial planner to confirm if an 83(b) election aligns with your overall financial goals and risk tolerance.

Rule #6: Tax Rates and Restricted Stock Units

Be sure to anticipate what restricted stock and RSUs will do to your tax rates when you vest.

The extra income could push your income into a higher tax bracket, raise your rate of capital gains tax, and trigger extra Medicare taxes, possibly costing you thousands of dollars. If you plan ahead, you can implement strategies that could keep you in the lower tax brackets.

When you hold restricted stock or RSUs, it’s important to understand their impact on both ordinary income and capital gains taxes.

Tax rates vary by state—some impose high income and capital gains taxes, while others charge little or none. Your location can significantly influence what you owe. Other factors, such as your total income, the length of time you have held the shares, and your filing status, also play a role.

Typically, the market value of your shares becomes taxable income when they vest, which may increase your federal and state tax burden. (Remember, if you made a Section 83(b) election for restricted stock, the income would have been taxed earlier.)

After vesting, any additional increase in the share price is usually treated as capital gains.

Selling shares within a year of vesting usually means paying short-term capital gains taxes at ordinary income tax rates (currently 10% to 37% federally).

Wait over a year, and you’ll generally qualify for long-term capital gains rates (currently 0% to 20% federally). Plus an additional 3.8% net investment income tax for those individuals with high income.

Please note: Tax laws and rates can change, and states may have unique rules that affect your final bill. To stay informed, it’s wise to keep track of any changes or work with a financial professional.

Rule #7: RSU Selling Strategy: Decide Whether to Hold or Sell

Whether or not you sell your shares at vesting will depend on multiple factors, such as tax planning, financial planning goals, and company restrictions.

If you sell immediately, you can use the shares to pay for the taxes incurred at vesting.

If you hold your shares, your capital gains tax will be affected when you sell in the future.

Your decision may be influenced by your cash needs, upcoming life events, and other financial planning factors, including diversification, dividends paid on your stock, and alternative investments.

If your company is publicly traded, there can be blackout dates that prevent you from trading and stock ownership guidelines that require you to keep a certain amount of stock. With private companies, there are probably restrictions in your grant or SEC rules that will impact when you can sell.

Rule #8: Remember Dividends

Even though you can’t transfer or sell restricted stock until it vests, the stock is still issued to you and in your name, which means you could receive dividends.

If you have unvested RSUs, this does not apply.

But when a company pays dividends on outstanding shares of stock, it can choose to pay dividend equivalents on RSUs. These may be deferred or accrued to additional units and then settled when the unit vests.

Rule #9: Don’t Let Company Stock Skew Your Portfolio

It’s a cliché, but when it comes to your portfolio, you don’t want to keep all of your eggs in one basket. You don’t want too much of your net worth tied up in your company stock, and since restricted stock and RSUs vest over time, it’s easy to miscalculate how much of your portfolio is reliant on the success of your company.

In order to avoid overconcentration, consider working with a CERTIFIED FINANCIAL PLANNER® to determine how much your holdings in company stock contribute to your overall net worth.

A financial advisor can help you tackle concentration risk by building a plan to gradually reduce your holdings in company stock.

Together, you might set up automatic sales when shares vest, look for opportunities to offset gains through tax strategies, or use hedging tools to manage volatility.

The proceeds can then be channeled into a well-diversified blend of broad-market funds, bonds, or alternative investments, reducing your reliance on a single stock’s performance. Ongoing reviews help make sure your approach stays in step with your goals, risk tolerance, and changes in the market.

With a more diversified approach, you won’t be betting your financial future on a single stock. And as life changes, regular check-ins will help you stay on track.

Rule #10: Rely on a Professional

Managing restricted stock, RSUs, and everything that comes with them can get complicated fast. From taxes to timing to investment decisions, there’s a lot to think about — and it’s easy to feel unsure about the best path forward.

That’s where we come in.

At Archer Investment Management, we help tech professionals navigate the ins and outs of equity compensation and build plans that align with their lives and goals.

If you have ESOs, restricted stock, or RSUs, don’t hesitate to reach out to us to help you maximize restricted stock units (RSUs) and incorporate them into your overall financial picture.

If you’re looking for clarity and a strategy that ties it all together and takes the guesswork out of managing your restricted stock, we’re here to help.

Selling your ISO shares too early (i.e. a disqualifying disposition) can very well mean that you’ll end up paying more taxes than if you had waited for a qualifying sale.

Timing matters: hold your shares for at least 1 year after exercise and 2 years after the grant date to get lower long-term capital gains tax rates.

Sometimes, selling early still makes sense if you need cash or just want to reduce risk (for example, if your company’s future feels uncertain).

An Important Decision: Should I take a Qualifying Disposition or Sell Earlier, Triggering a Disqualifying Disposition?

If you’re a tech professional who has received Incentive Stock Options (ISOs) from your employer, one of the biggest financial decisions you’ll make is deciding when to sell your shares after you’ve purchased them (a step known as exercising).

Exercising ISOs presents a critical decision: Should you aim for a qualifying disposition or selling earlier, triggering a disqualifying disposition? The choice isn’t just about taxes; it can play a role in your financial goals, such as buying a home or managing risks in your portfolio.

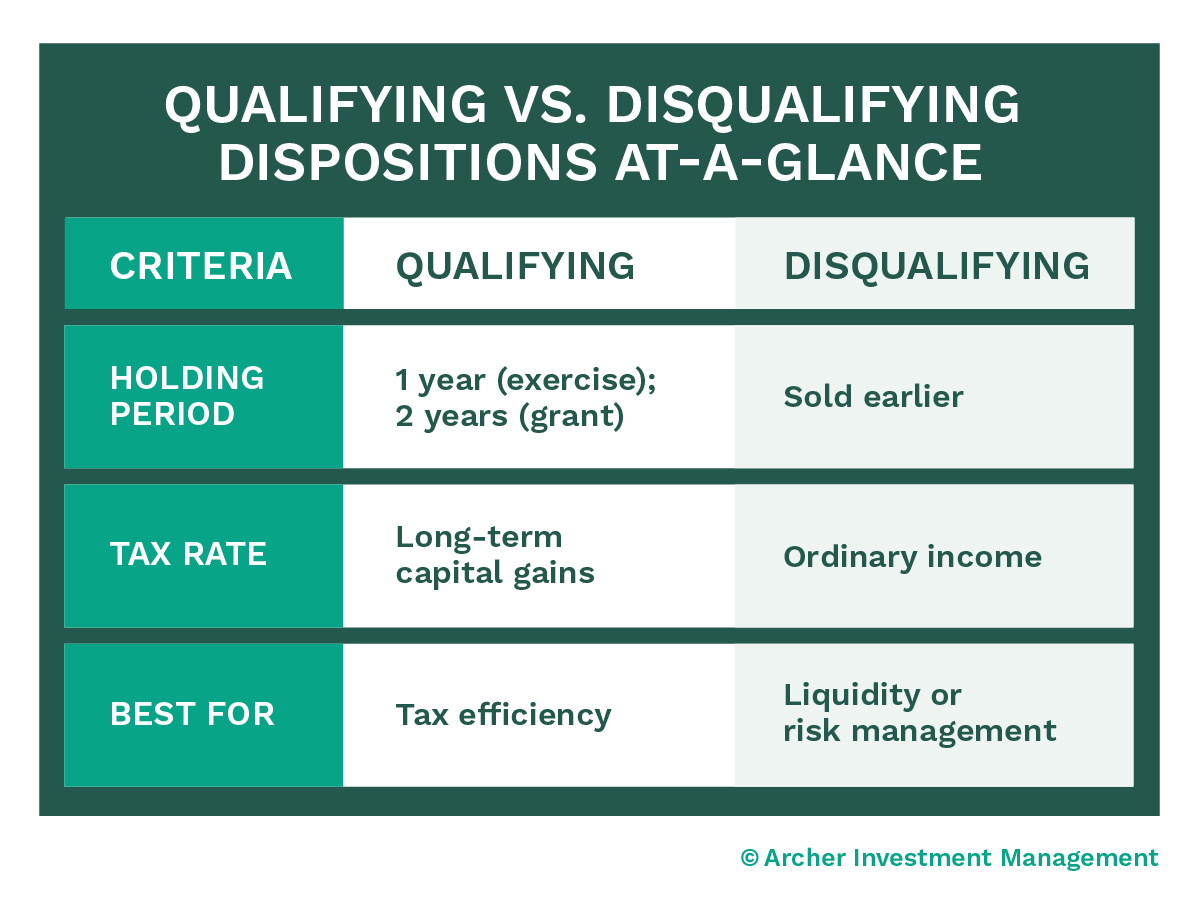

What Are Qualifying and Disqualifying Dispositions?

Qualifying Disposition

A qualifying disposition happens when you sell your ISO shares after meeting two specific holding period requirements:

1. At least one year after the exercise date (when you purchased the shares)

2. At least two years after the grant date (when you received the options)

When you meet both of these requirements, you’ll pay the lower long-term capital gains tax rate (0%, 15%, or 20%, depending on your income) instead of the much higher ordinary income tax rates.

Watch Out! Many people only focus on the one-year holding period after exercise. But don’t forget—you also need to hold them for at least two years after the grant date. Missing this second requirement could mean paying much higher taxes by triggering a disqualifying disposition.

Disqualifying Disposition

A disqualifying disposition happens if you sell your ISO shares too early—before meeting the two holding periods.

When this happens, your profits are taxed at ordinary income tax rates, which can go as high as 37% for top earners. That’s a big difference from the lower rates when the sale is considered a qualifying disposition.

Viewing ISOs and Employer Shares from a Portfolio Perspective

It’s exciting to hold stock in your company, but holding too much can be risky. If the stock price drops, your portfolio could take a big hit.

That’s why it’s important to think about your ISOs as part of a bigger picture and make sure your investments are well-balanced to protect your long-term financial health.

The Real Tax Impact: Why It Matters

The difference between qualifying and disqualifying dispositions has a big impact on how much of your profit you get to keep after taxes.

Here’s the breakdown:

Qualifying Disposition: You’ll pay the lower long-term capital gains rate (around 15-20% for most people).

Disqualifying Disposition: You’ll pay the higher ordinary income tax rate, which can reach up to 37%.

Let’s say you’re in the highest tax bracket. The difference between these rates could mean paying 17% more in taxes—potentially costing you tens of thousands of dollars, depending on how much stock you’re selling.

Struggling to untangle the best time to sell your stock? That’s exactly what we help our clients with every day. Schedule a call with us, and we can help you figure it out.

When a Disqualifying Disposition Might Make Sense

Even though disqualifying dispositions can come with higher taxes, there are times when they make good financial sense.

If you have immediate liquidity needs—whether for buying a house, paying for an emergency, covering education costs, or any other major expense—having money on hand might be more valuable than holding out for tax savings.

Selling early can also help reduce your financial risk.

For example, if you’re worried about your company’s performance, stock market swings, or your own job security, it could be smarter to sell some shares now and diversify your investments rather than waiting just to save on taxes.

Here’s a real-life example: One of our clients, a Tesla employee, faced an unexpected layoff. They needed money quickly to relocate, buy a bigger home, purchase a second car, and prepare for a baby.

In this situation, selling the shares immediately—even with the higher tax hit—was the right move.

The immediate funds allowed them to meet their needs without unnecessary stress.

If you exercise your ISOs but don’t sell the shares right away, you might owe AMT even though you haven’t made any money from selling them.

Here’s how it works: The IRS looks at the “paper gain”—the difference between the price you paid to exercise your options and the market value of the stock. Even if you’re just holding the shares, this paper gain can create a tax bill. It’s one more thing to factor in when planning your ISO strategy.

A paper gain is like potential profit. It’s the difference between what you paid for your stock when you exercised your options and what the stock is worth today.

Even though you haven’t sold the stock or made any real money, the IRS looks at this potential profit and might tax you on it with the Alternative Minimum Tax (AMT). It’s like being taxed on money you don’t actually have in your pocket yet!

(We often refer to this potential profit as “an “unrealized” gain).

Five Key Considerations for Deciding When to Sell Your ISO Shares

There’s no one-size-fits-all answer for when to sell your ISO shares—it all depends on your personal situation and financial planning needs.

Start by looking at your income level. If you’re in a higher tax bracket, the tax difference between qualifying and disqualifying dispositions becomes even more important.

Next, think about market risk. Waiting to meet the waiting requirements for a qualifying disposition might save on taxes, but it also means holding onto your shares longer. If the stock price drops during the holding period, those tax savings could disappear.

To stay on top of things, make sure you keep track of key dates such as your grant date, exercise date, and vesting schedules. Knowing these details can help you plan your sales effectively.

A great strategy to lower risk is “staged selling.” Instead of selling all your shares at once, sell in smaller amounts over time. This approach balances market risk with tax benefits.

Lastly, check how much of your portfolio is tied up in employer stock. Too much can leave you overexposed if your company’s stock takes a hit. Diversifying your investments is key to long-term financial stability.

Remember, tax laws aren’t set in stone

Tax laws change, which could affect how you plan your ISO sales. Changes to capital gains tax rates or AMT rules might also impact your strategy.

To make informed ISO decisions, take a close look at your grant dates and exercise dates, calculating the tax impact of a qualifying versus selling early to trigger a disqualifying disposition, and consider any immediate liquidity needs. Your risk tolerance also shapes your approach.

Once you have a clear sense of your financial picture, set a timeline for exercising and selling your shares based on the current market and your company’s performance.

Qualifying dispositions can be a great way to save on taxes, but they’re not always the right choice. The best decision balances tax savings with your personal needs and financial goals.

Sometimes, it’s worth paying a little more in taxes if it helps you meet a big life goal, reduce risk, or feel more financially secure.

Get Financial Tips, Insights, and Resources delivered to your inbox

We honestly could not ask for a better partner.

My husband and I have been working with Richard and the team at Archer Management Group for over 10 years, and we honestly couldn’t ask for a better partner. Richard is not only incredibly knowledgeable — he’s also just a genuinely great person. We always feel like he’s looking out for us and helping guide us in the right direction. He’s helped us through an inheritance, purchasing homes, managing complex stock options/RSAs at work and helps keep our finances running smoothly.

The whole team is super responsive and on top of things, and they’ve made the whole process of managing our finances feel less stressful and more secure. We really trust Richard with our money, and that peace of mind is huge for us. I highly recommend Richard and team!

Dave

Received on Google July 2025

These testimonials were provided by current Archer Investment Management clients and may not be representative of the experiences of other clients. The clients were not compensated, nor are there material conflicts of interest that would affect the given testimonials. You can view a complete list of reviews at Emily Rassam’s and Richard Archer’s Wealthtender profiles.

Most thorough and personable financial planners and wealth managers

George and I had been with an investment firm that promised many things they never got to deliver. We are so grateful to have found Archer Investments. Emily,Richard and all of the staff are extremely knowledgeable and so personal. We feel like family to them.We also feel so comfortable with our financial planning that has transpired, feeling confident in our long range plans, short term goals, the security of having ample insurance and medical coverage along with complete documents (POA’s, wills, healthcare POA’s, everything to make any transition smooth for our family). It is a tremendous relief to have everything in place. Their wealth of knowledge and attention to detail is impeccable. We feel so blessed to have found them and highly recommend their comprehensive services.

Andrea & George

Received via WealthTender: April 4, 2024

Comprehensive financial planning

Working with Emily, Richard, and the team has been great! Their insight has been invaluable for me across a variety of domains. Their approach builds from goals backwards — we met together to outline short and long-term goals and then used those goals to create a plan across a variety of decisions, from home ownership to car insurance to investment and much more. Richard and Emily truly do a great job of drawing me into the loop, ensuring that the financial plan we develop reflects my goals and wishes. Before settling with Archer Investments, I talked with a number of other advisors and none of them had the combination of professionalism, attention to detail, and comprehensive services offered by Archer.

Ben

Received via WealthTender: July 1, 2024

I was quite literally afraid of getting help and of all that it involved. It’s been wonderful. No kidding: best decision ever!

I’m not finance-oriented by any measure, but luck came my way for once and I found myself having enough assets to need some help. Only I didn’t know what kind of help I needed and it’s easy to get overwhelmed quickly and I was on like year number whatever of being overwhelmed and I just kicked that can down the road every year. After a short search, I found Archer’s team and quickly just pushed other options off the table and signed on. They’ve actually been able to simplify things in a way that makes me feel like I can manage my life and not worry about it all for the first time in years. I basically had all eggs, but no basket. Now I have a comprehensive plan from some incredible staff and I actually love the process instead of dreading the matter. Simply put, Archer has changed how I view my own finances and what used to be a cause of stress for me is now a giant sigh of relief. I said in the title it was the best decision ever and I mean it: this has 100% seriously no-fingers-crossed changed my life. If you’re like me and you’ve been debating if you even need this kind of help, then yes… yes, you do!

Scott Eaton

Received via WealthTender: July 10, 2024

We honestly could not ask for a better partner.

My husband and I have been working with Richard and the team at Archer Management Group for over 10 years, and we honestly couldn’t ask for a better partner. Richard is not only incredibly knowledgeable — he’s also just a genuinely great person. We always feel like he’s looking out for us and helping guide us in the right direction. He’s helped us through an inheritance, purchasing homes, managing complex stock options/RSAs at work and helps keep our finances running smoothly.

The whole team is super responsive and on top of things, and they’ve made the whole process of managing our finances feel less stressful and more secure. We really trust Richard with our money, and that peace of mind is huge for us. I highly recommend Richard and team!

Dave

Received on Google July 2025

×

Their expertise in the tech startup industry is invaluable to navigate company stock options and instill confidence when exercising.

Working with Emily, Richard, and the rest of the Archer team has been an absolute game-changer for my financial well-being. From our very first meeting, their friendliness and professionalism put me completely at ease. I feel like they genuinely care about my goals, and they’ve been incredibly patient in answering all my (many!) questions. If you are anything like me starting this process with no idea what the heck your financial goals are, don’t worry, they will gently guide you. They do a thorough intake process over several meetings to identify goals, risk tolerance, and get to know clients.

I had a scattered mess of accounts due to changing employers and random investments over the years. Now all of those accounts are organized and manageable from a single place. Their expertise in the tech startup industry is invaluable to navigate company stock options and instill confidence when exercising. What truly sets them apart is their high quality tooling. I love love love that they have everything in a secure cloud with custom dashboards, and all signatures are electronic – no more printing and mailing, thank goodness! They also pre-fill any necessary forms with my personal info which is a huge timesaver. Their responsiveness is truly remarkable; I’ve always received incredibly fast replies. This level of dedication is rare and greatly appreciated. Last but not least, I get to sit back and watch my investments grow. For the first time in my life, I can see a path to early retirement.

I wholeheartedly recommend Archer Investment Management to anyone seeking a trustworthy, knowledgeable, and highly responsive financial planning service.

Maggie

Received on Google May 2025

×

Personalized to our lifestyle

Richard and Emily are a fantastic team! We reached a point in our life that we thankfully had options for our money, investments, and the way we wanted to live our lives. Their approach is personalized to understand your relationship with finances and tailored to how you want to enjoy your money now and into the future. We had considered ourselves smart with our finances, but the Archer team exceeded our expectations and opened up several opportunities to maximize our potential. We got support & recommendations for exactly how to allocate, invest, and yes spend our money the way we wanted our lifestyle to be. This approach gave us the peace of mind knowing our future was secure, our 3 kids college was within reach, and our “fun” spending on family and vacations was a balanced way for us to enjoy the long journey. And on top of that, they make the process simple and as easy as possible. So glad we found this team.

Danny and Julia

Received on WealthTender October 2024

×

I was quite literally afraid of getting help and all that it involved. It’s been wonderful. No kidding: best decision ever!

I’m not finance-oriented by any measure, but luck came my way for once and I found myself having enough assets to need some help. Only I didn’t know what kind of help I needed and it’s easy to get overwhelmed quickly and I was on like year number whatever of being overwhelmed and I just kicked that can down the road every year. After a short search, I found Archer’s team and quickly just pushed other options off the table and signed on. They’ve actually been able to simplify things in a way that makes me feel like I can manage my life and not worry about it all for the first time in years. I basically had all eggs, but no basket. Now I have a comprehensive plan from some incredible staff and I actually love the process instead of dreading the matter. Simply put, Archer has changed how I view my own finances and what used to be a cause of stress for me is now a giant sigh of relief. I said in the title it was the best decision ever and I mean it: this has 100% seriously no-fingers-crossed changed my life. If you’re like me and you’ve been debating if you even need this kind of help, then yes… yes, you do!

Scott

Received on WealthTender July 2024

×

Most thorough and personable financial planners and wealth managers.

George and I had been with an investment firm that promised many things they never got to deliver. We are so grateful to have found Archer Investments. Emily,Richard and all of the staff are extremely knowledgeable and so personal. We feel like family to them.We also feel so comfortable with our financial planning that has transpired, feeling confident in our long range plans, short term goals, the security of having ample insurance and medical coverage along with complete documents (POA’s, wills, healthcare POA’s, everything to make any transition smooth for our family). It is a tremendous relief to have everything in place. Their wealth of knowledge and attention to detail is impeccable. We feel so blessed to have found them and highly recommend their comprehensive services.

Andrea and George

Received on WealthTender 2024

×

We’ll forever remember Emily as the person who said we could retire.

We’ve worked with Emily for a few years now, and have been so impressed. She is a wealth of knowledge and a way of being able to answer a lay person’s questions in a very thorough and understandable manner. She can answer any question you throw at her with detail and clarity. She is honest, credible and trustworthy. She is very knowledgeable about the technology she has available to use and is able to provide strong visuals and projections to help with making decisions. She is always willing to meet and discuss a given topic or to provide an update on our portfolio. We’ll forever remember Emily as the person who said we could retire. That’s a hard decision to make and she was able to clearly show us the path. I’d highly recommend Emily to work with as a Financial Advisor.

Kay

Received on WealthTender June 2022

×

There is no one else I would trust with my financial future. This advisor/client relationship is the best I’ve ever had.

Emily has been a lifesaver for me in so many ways. I needed a Financial Advisor that I could trust, and I could not be more pleased. She is honest, provides great advice, guidance and always goes the extra mile for her clients. She is always professional, knows what is going on in the industry and what services the company offers I could benefit from. I retired at the end of 2018, but before I did, I met with Emily, and we went over what my retirement would look like. There is no one else I would trust with my financial future. This advisor/client relationship is the best I’ve ever had. She keeps me on the right road! I appreciate her so much.

Elaine

Received on WealthTender June 2022

×

The entire experience has brought us a great sense of security

My wife and I have been with the Archer team for almost 3 years. Throughout, they have been responsive, thorough, and professional. All of the staff are excellent communicators, in person or via email/texts! The entire experience has brought us a great sense of security – from the initial “get to know you” conversations, with Rich doing an excellent job of listening, to the mid-course corrections when life changes. Initially they brought great organization to our portfolio, and our retirement is organized and easy to track. Whenever it’s time for us to do some homework, they are great at helping us with our end of the tasks.

Karen

Received on WealthTender February 2023

×

Before meeting with the Archer Team, we had concerns about the value wealth management would bring to the table. Those concerns were quickly squashed after meeting with the team.

We have really enjoyed working with Archer Investment Management. We reached out to them because we wanted financial guidance and reassurance as we move toward reaching education goals for our children and retirement goals for ourselves. We knew we needed to diversify some of our assets but had no idea how to do so in a financially savvy way. Before meeting with the Archer Team, we had concerns about the value wealth management would bring to the table. Those concerns were quickly squashed after meeting with the team. They pointed out things we hadn’t thought of and questions we hadn’t asked ourselves to help create more specific goals than we would have set for ourselves. They kindly and patiently walked us through creating a plan that fit our comfort level and helped us take the steps needed to put that plan in action. If any of this sounds overwhelming, I can’t reiterate enough how much patience and support we received. It never felt overwhelming. We are so relieved to now have the support of these specific experts to help us stay on track to hitting our goals.

What the Tax Picture Could Look Like

What the Tax Picture Could Look Like The State-Tax Swing: Why Residency Matters in SpaceX IPO Planning

The State-Tax Swing: Why Residency Matters in SpaceX IPO Planning

IPO Wealth Is a Life-Planning Moment

IPO Wealth Is a Life-Planning Moment